Português

Português  Русский

Русский English

English Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Os legisladores americanos estão perdendo o controle do rápido progresso da reforma fiscal através do Congresso, e se esqueceram completamente a questão de quem pagará pelo banquete? Reduzir impostos e aumentar o déficit orçamentário requer um aumento na emissão de obrigações de dívida. Nas compras deste último, em geral, os não residentes estão envolvidos, sendo o maior deles o Japão e a China. Eles geralmente pagam pelo brilhante futuro da economia dos EUA. A este respeito, torna-se claro por que a informação sobre a redução dos juros em títulos dos EUA pela China produziu o efeito bomba nos mercados financeiros.

Pode-se, é claro, argumentar por muito tempo que papel na declaração de Pequim que "tem ativos mais atrativos" atuou nos ataques de Donald Trump contra a China, mas o fato é que: se o Império Celestial reduzir sua presença no mercado de dívida dos EUA, o benefício para o dólar não vai acabar. E o dólar "americano" imediatamente reagiu às notícias da Ásia com uma queda rápida, o que permitiu que as cotações de futuros do ouro restaurem as posições perdidas nos dias anteriores e passem a cerca de US $ 1325 por onça.

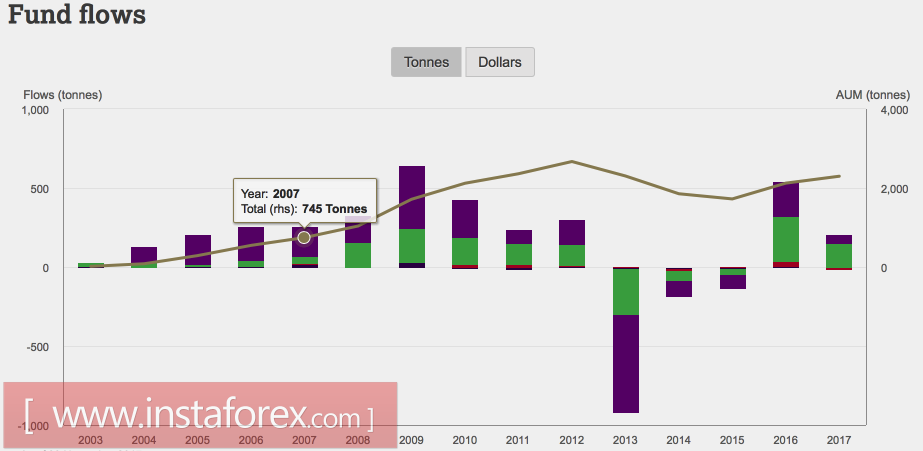

O metal geralmente se comporta de forma bastante inesperada, cada vez que marca o crescimento, o próximo aumento da taxa em fundos federais. Ao mesmo tempo, o fortalecimento do euro em 14% em relação ao dólar norte-americano em 2017 foi paralelo ao crescimento do interesse em produtos focados no ETF dourado. 75% do fluxo líquido de capital foi atribuído aos fundos europeus (+148,6 toneladas), enquanto que a Alemanha representou 35%. O ETF asiático, ao contrário, representou 54% da saída de capital bruto. A questão é, se a China perdeu o interesse pelo ouro e por títulos norte-americanos, o que ele vai comprar? A resposta correta fará um bom lucro.

Dinãmica de fluxo de ativos fixos en ETF

Source: WGC.

Thus, Donald Trump needs to think three times before continuing to roll barrels to the largest countries of Asia, especially since Japan is also able to respond. The announcement that BoJ reduces purchases of long-term bonds in January, became the catalyst for the collapse of USD / JPY. This pair in recent months quite synchronously moved with gold, so the rumors about the normalization of the monetary policy of the Bank of Japan can be perceived as a "bullish" factor for the precious metal. Indeed, in this scenario, the chances of the USD index to restore the uptrend are zero, and the weakness of the dollar was traditionally perceived as a favorable external background for XAU / USD fans.

It is curious that gold is an asset-refuge, which usually falls into a wave of sales in the event of accelerating global GDP. This time, the precious metal rally coincided with an increase in world economic growth forecasts by the World Bank to 3.1% in 2018. According to the authoritative organization, for the first time since 2008, it will exceed its potential level. The reason for the deviations from the historical connection of the precious metal with global GDP should be sought in a weak dollar.

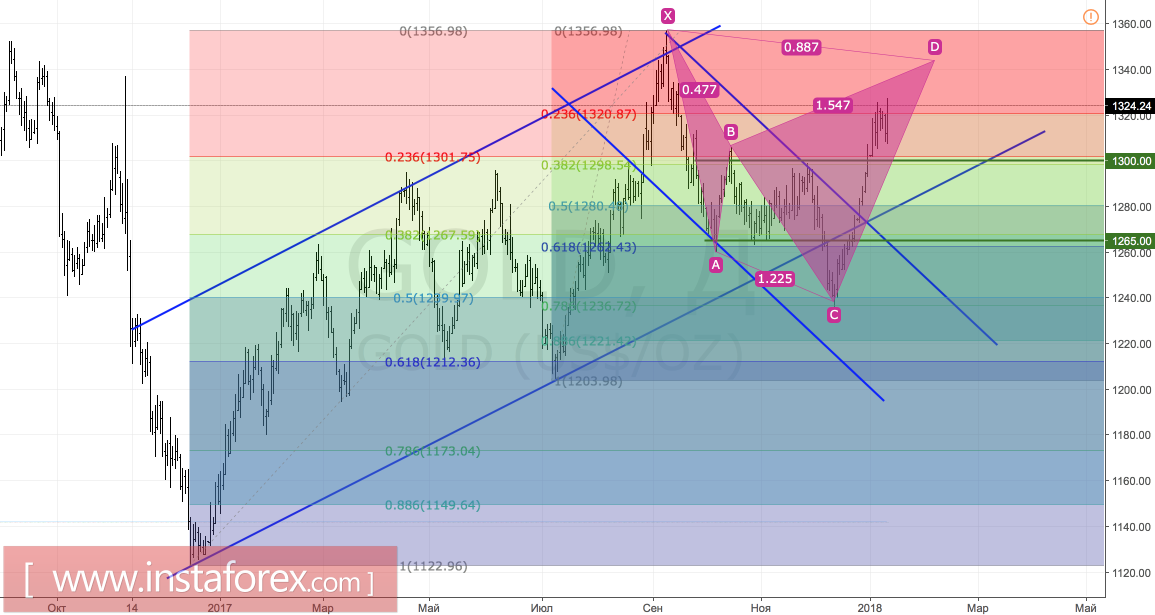

Technically, if the bulls on the analyzed asset manage to gain a foothold above the important level of $ 1321 per ounce, the risks of implementing the target by 88.6% on the pattern of the "Shark" will increase.

Gold, daily chart