English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Eurozone

The GDP growth in the euro area for the second quarter was slightly higher than expected. the adjusted annual growth estimate increased from 2.1% to 2.2%, which supports the euro.

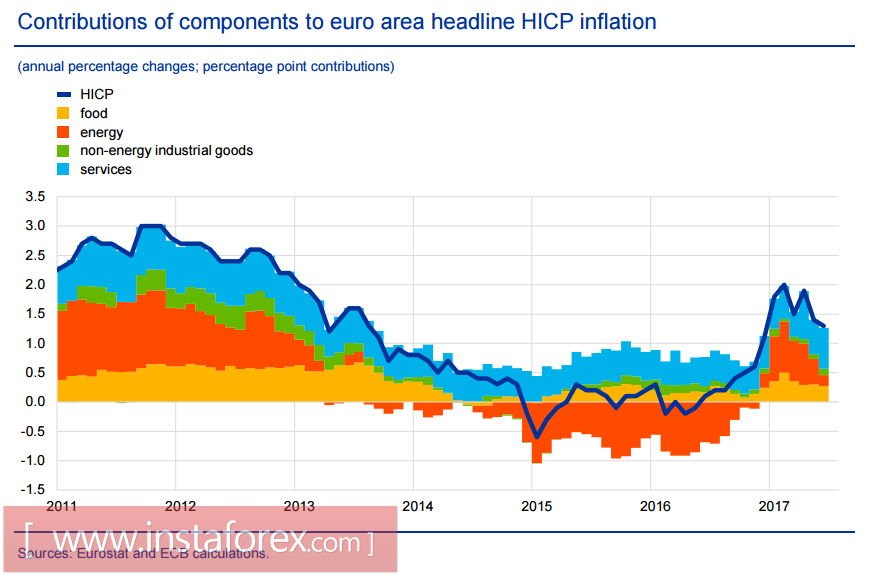

According to the published report in August from the economic bulletin, there was a slowdown in the inflation for the second quarter but it is sure that the problem is only in the reduction of energy prices and partly in food products. The basic level of inflation remains confidently high, although this point seems rather controversial. As can be clearly seen in the graph below, the prices of the services sector were the main reason. The price dynamics of the group of industrial products in the non-energy sector has a noticeable lower price growth compared to the period of 2011/13 when the deflationary pressure on still quite strong.

The volume of imports of goods has declined and has become pronounced in the second quarter that has slowed down the global trade. This increases the likelihood of the publication of today's report on inflation from the euro area to show a more significant price deceleration than the market expectation and initiate a sell-off of the euro.

The ECB minutes of the meeting is also expected to be published today, which will be considered by the traders to look for possible hints in the internal discussion regarding the timing of the easing of the incentive program. Recent trends indicate that the concern of the ECB may even increase, as the industry and the export-oriented sector of the economy are under threat because of simultaneous pressure from several sides. In these conditions, there is no need to wait for hints to reduce the incentive program since the protocol will help to weaken the euro.

The likelihood of a correctional decline in EUR/USD pair is growing. Following the results of the week, the pair may fall to 1.1650 amid a reduced geopolitical risks and weak statistics from the USA.

United Kingdom

The British pound has declined in reaction to weaker than expected data on consumer inflation. The price decrease in July was 0.1% with a year-on-year growth of 2.6%. Both indicators are worse than forecast.

At the same time, there are some positive points. The index of retail prices rose more than expected while the report on the labor market, published on Wednesday, showed a positive trend in most parameters. Applications for benefits have decreased in number and the unemployment rate also decreased from 4.5% to 4.4%. On the other hand, the average wage increased by 2.1%, which was better than forecasts and the level attained in June.

The latter parameter can serve as the basis for optimism since it will contribute to the growth of inflation, which also increases the probability of a rate hike by the Bank of England. This factor will give some support to the pound.

The data on retail sales for the month of July will be published today which can induce the market to move in any direction. Although expectations are moderately negative, experts expect weaker indicators than a month ago.

The pound continues to be under pressure, despite the fact that bulls on the dollar will not get together for a full-fledged offensive. The move towards 1.28 followed by a slide to 1.25 will most likely happen than the resumption of growth.

Oil

Commercial crude oil inventories from the U.S. fell by 1.9%, or 8.9 million barrels. The decline has significantly exceeded the forecasts of experts. Oil reacted with growth but a number of other indicators had a pronounced bearish sentiment, which eventually led to a decrease in quotations. At this time, the main forecast is the next increase in production amounts to 79 thousand barrels per day, or 0.84%. Next month, oil production in the U.S. could reach a record level, which could eventually lead to the blocking of OPEC measures and will further lower quotations. Furthermore, the cost of production in the U.S. is increasing, that leaves the production growth to be questionable in the coming months.