English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

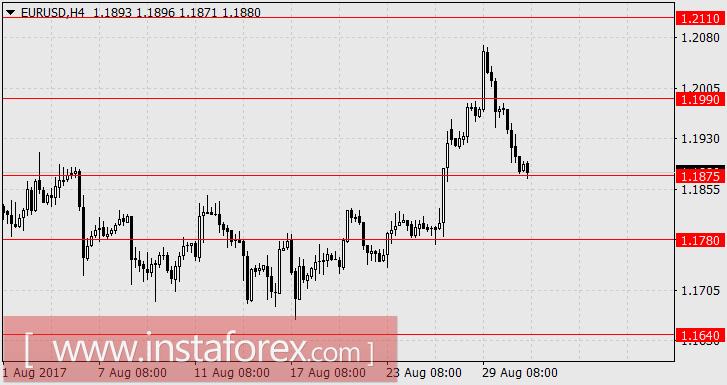

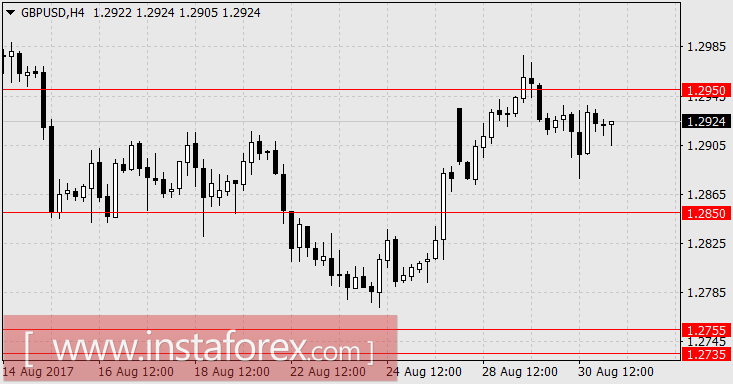

EUR / USD, GBP / USD

The main market driver yesterday is the second estimate of US GDP for the 2nd quarter which met its expectations. The revision raised its estimate from 2.6% to 3.0% with an expectation to increase by 2.7%. In the form of GDP, consumer spending showed an increase of 3.3% against the initial estimate of 1.9%, while business investments rose by 0.6% against 0.4% in the previous estimate. The ADP released a report about the creation of 237,000 new jobs in the private sector in August against the expectation of 185,000, with an upward revision from 178,000 to 201,000 in July. As expected, this significant increase causes investors to have higher estimates than the original forecast with Friday's 180K non farm payroll report

Nevertheless, the euro and the pound began to decline during the day, as the consumer prices in Spain came in at 1.6% YoY, which is lower than the anticipated 1.7% YoY. While the expectation of the decline in European inflation is 11.6 versus 11 and the initial forecast of 7. The UK lending also weakens in July, showing the GBP at 5.5 billion down to 4.8 billion pounds from the 5.6 billion initially, with the anticipation of 5.3 billion. Mortgage lending also showed a contraction of 3.6 billion pounds against 4.1 billion in June, against the forecast of 3.5 billion. However, the number of approved applications for mortgages showed an increase from 65.3 thousand to 68.7 thousand.

Mass media continues to intimidate the public with the "prohibitive" euro exchange rate. The CNBC Business News Channel issued an interview with the director of the Center for European Policy Studies about the roll-out of export-oriented countries into recession in case of continuous growth of the euro. In connection with this issue, we see the resolute intention of large investors to buy dollars, as the speculative degree of purchases is clearly high.

Today, investors' attention will focus on the inflationary indicators of the euro zone and on US consumer spending. The base CPI of the euro zone for August is projected to remain unchanged at 1.2% YoY, while the total CPI is expected to increase from 1.3% YoY to 1.4% YoY. The monthly increase in France's CPI is expected to be at 0.5% vs -0.3% in July, while in Italy the growth is expected to be 0.2%. For other indicators of the euro zone, expectations are less optimistic as the German retail sales may fall by 0.4%, while in Spain retail sales may slide down from 2.5% YoY to 2.4% YoY. The number of unemployed in Germany is expected to decline by 6,000, but this may not affect the change in the unemployment level. The unemployment forecast in the euro zone as a whole for July is 9.1%.

In the US, personal income for July is expected to increase by 0.3% vs. 0.0% a month earlier, as consumer spending is expected to grow by 0.4% against 0.1% in June. The business activity index in the manufacturing sector of the Chicago region in August is projected to decrease from 58.9 to 58.7, the unfinished housing sales for July may increase to 0.4% after the previous growth of 1.5%.

The balance of indicators, even without considering the general background of "dangerously expensive euro", is in favor of the dollar. We are expecting for the euro at 1.1780 and pound sterling awaits in the range of 1.2735 / 55.

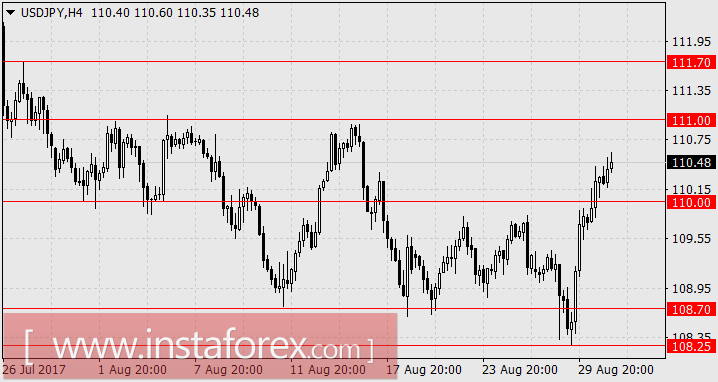

USD / JPY

In the latest review of the yen, it is not expected that the emergence of factors could sharply deploy this currency market. But, a sharp turn in the assessment of the current euro exchange rate by the business press is also unexpected. The Japanese yen was rescued again by the American stock market, as the yen gained 46 points (from the day's minimum the growth was 16 points) on Tuesday. On Wednesday, the growth was 50 points. Yesterday, Nikkei 225 increased by 0.74%, and today, the main Japanese index acquired 0.73%. The American S&P500 rose by 0.46% on Wednesday. The Japanese economic data did not remain indifferent since the annualized rate of retail sales in July showed an increase of 1.9% against the forecast of 1.0%. The previous indicator was 2.1% YoY. The dispersal of the yen was really strong that even the flat data of July industrial production released today was unable to stop this growth. Industrial Production showed -0.8% surge against the forecast of -0.4%. But the high previous growth of 2.2% could ease the situation. Furthermore, the Chinese manufacturing activity index for August showed an increase from 51.4 to 51.7 against expectations of a decline to 51.3. The non-production PMI of China decreased - 53.4 against 54.5 before.

In Europe, the press hurried to support the Japanese market because the business media have various articles regarding the unimportance of political conflict in the latest ballistic missile launch of North Korea, in spite of this, North Korea had already sent off several launches and nothing had happened. Meanwhile, the whole trade robots did not adequately respond to the headlines in the newspaper. Even the yields on Japanese government bonds went up. We are expecting for the yen at 111.70.