English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

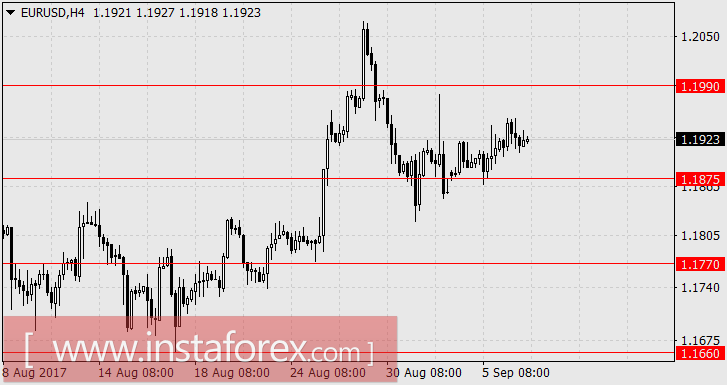

EUR / USD, GBP / USD

The main event of yesterday was an unexpected rate hike by the Bank of Canada of a quarter point to 1.00% against the expectations of the markets for the rate to stay. Canada's trade balance for July, however, improved from -3.8 billion dollars to -3.0 billion with expectations at -3.2 billion dollars. The strengthening of the "Canadian dollar" by one and a half figures did not happen but it put pressure on the US dollar against other currencies. Despite this, the European data came out worse than the pessimistic forecasts. The volume of industrial orders in Germany fell by 0.7% in July, with the expected growth of 0.2% against the previous growth of 0.9% (revised down from 1.0%). Business activity (PMI) in the retail sector of the euro area decreased from 51.0 to 50.8. Retail sales in Italy for July showed 0.2% against expectations of 0.4% and the June growth of 0.6%.

However, the US PMIs did a little piss. According to Markit, the final evaluation of Services PMI in August was 56.0, against expectations of 56.8 and 56.9 for the month before. The ISM Institute's evaluation of non-manufacturing PMI presented 55.3 points against the forecast of 55.8. The trade balance of the US came out slightly better than the forecast: -43.7 billion dollars against -44.6 billion. In general, the euro closed the day with a 4 point growth and the British pound with a 10 points addition. And, of course, two of the strongest hurricanes in two weeks that hit the US became a bit much. Hurricane Irma is approaching Florida. Counterweight to these unfavorable factors for the dollar is geopolitical tensions. US Treasury Secretary S. Mnuchin said that if the UN refuses to impose sanctions on North Korea, the United States can unilaterally impose sanctions on any country that trades with the DPRK. Traditionally, hurricanes subsequently have a stimulating effect on the labor market. The "Beige Book" defined economic growth as moderately slow, drawing attention to the lack of skilled labor.

Today, the main event will be the decision of the ECB on monetary policy and the subsequent press conference of its head, Mario Draghi. It is expected that there will be no statements about curtailment of incentives because such an announcement is expected in October. Accordingly, we do not expect strong movement in the euro. In the afternoon, the July industrial production of Germany will be released with a forecast of 0.6%. In connection with yesterday's failure on industrial orders, it is very likely that the indicator will be worse. France's trade balance is expected to correct the negative balance: a forecast of -4.5 billion euros against -4.7 billion earlier. The GDP of the eurozone for the second quarter is forecasted at 0.6%, as in the previous period (2.2% y / y). In the US, labor costs in the second quarter for the final estimate are expected to decrease to 0.5% from 0.6%.

In general, we see a balance of fundamental incoming data for the dollar. The main scenario is trading in the range of 1.1875-1.1990, followed by a decrease to 1.1770 due to the Congressional decision on the state debt limit and the Fed meeting. Breaking this balance may cause Mario Draghi to once again verbally affect the "high" rate of the euro. In the UK on Friday, good data is expected which can keep investors in a positive mood. We assume growth in the range of 1.3095-1.3115.

The resignation of Deputy Chairman of the Federal Reserve Stanley Fischer strengthens the uncertainty of the market and the horizontal trend. His powers were determined to last until July 2018, but Fischer will leave early in mid-October.

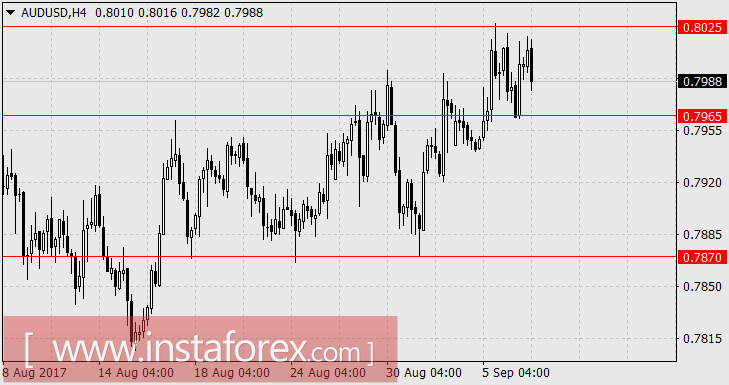

AUD / USD

For the third day of the week, the Australian dollar is trading in the range of 0.7965-0.8025. On Wednesday, GDP for the second quarter showed growth slightly below the forecast: 0.8% against 0.9%. In the previous period, growth was 0.3%. In annual terms, GDP added 1.8% against expectations of 1.9% and 1.7% y / y in the 1st quarter. Today, the figures came out significantly worse. The trade balance for July decreased from 0.888 billion dollars to 0.460 billion while waiting for 0.875 billion dollars. Taking into account that the June volume was raised from $ 0.856 billion, the forecast suggested an increase in Trade Balance, but the market met a decline. Export lost 2.0% while imports decreased by 1.0%. The index of activity in the service sector by the version of AIG in August fell from 60.5 to 55.3. Retail sales for July showed zero growth against expectations of growth of 0.3%.

Iron ore lost in value 3.09% ($ 75.35) yesterday. The growth of oil appears to be a short-term phenomenon only because of hurricanes, as world production increases and the production of shale oil in the US sets historical records.

We are waiting for the price to return to 0.7870.