English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

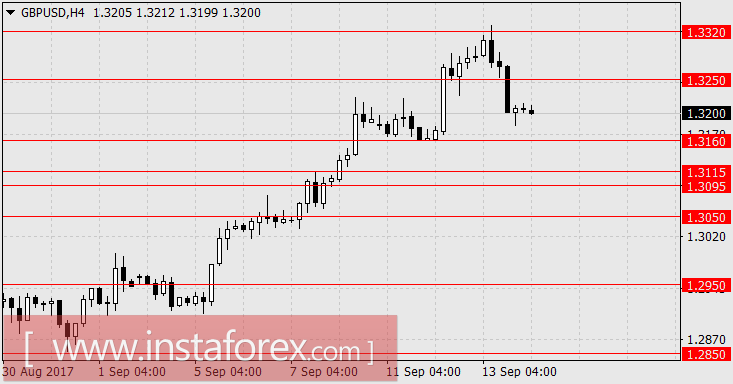

EUR/USD, GBP/USD

The market made further surprises and was able to anticipate the future yesterday. It seems that market environment is calm and strong movements are only expected on the day of Bank of England meeting, however, the British pound managed to disperse the dollar purchases.

With the release of UK employment data, which came out mixed as a whole, the pound began to decline in discrete increase every hour. Formally, the fall began because of the growth in wages which is slightly below the forecast of 2.1% within three months against expectations of 2.3%. But the number of unemployed fell by 2.8 thousand against expectations of growth by 0.8 thousand, and the jobless rate also dropped from 4.4% to 4.3%. Under normal conditions, the pound could not lose the whole figure with such data, as we see a mass closure of positions prior the World War II meeting. Meanwhile, when the pound continued to fall, the information regarding the nearly prepared budget agreement to be published next week was received by US Senator J. Manchin and head of the House of Representatives Committee on Budget K.Brady. The dollar waited the day that the euro will fell by 80 points. The support for the euro was weak, as the industrial production of the eurozone in July gained the expected 0.1% after the previous collapse of -0.6%. The employment rate in the euro area for the 2nd quarter increased by 0.4% against expectations of 0.3%. American indicators also showed weak growth, as the base producer price index for August showed + 0.1% against expectations of 0.2%, the general producer price index grew by 0.2% against the forecast of 0.3%.

In general, the political forecast and the associated growth in the dollar were justified. Donald Trump went on a compromise with the fulfillment (not without the strongest pressure from him) on most of his projects and ambitions, and only then the threshold of the national debt was defrozen in an operative manner and an agreement suddenly passes along the budget. Now, the probable long-term strengthening of the dollar, as it should be "strong America" (below parity).

Undoubtedly, the main event of the day will be the Bank of England's decision on monetary policy and the remarks of Mark Carney. The latest data on British inflation aroused the markets with the expectation of an earlier rate hike, but the oil market events are unfolding in such a way that oil prices may soon fall along with the inflation. It appears that the Bank of England will consider this factor of not making any hasty statements. Accordingly, we are waiting for Mark Carney's flat speech and the decline of the British currency.

The US consumer price index (CPI) for August and the forecast for the base index is 0.2%, for a total of 0.3%.

We are waiting for the British pound in the range 1.3095-1.3115 and the euro at 1.1770.

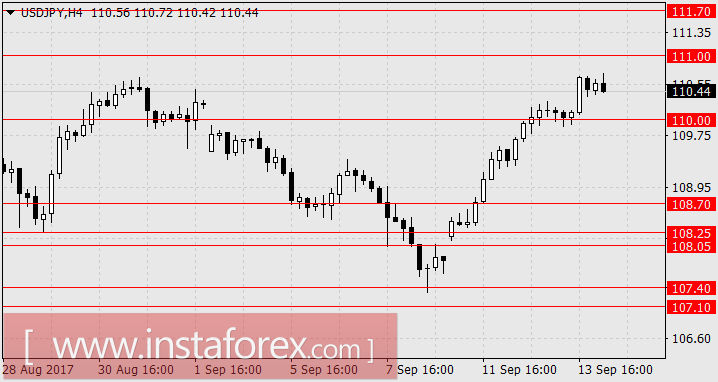

USD/JPY

As we noted in the previous review of the yen, the Japanese currency has only one risk to decline but was avoided, as the dollar and its markets weakened that brought great joy to the Japanese investors. Yesterday, the BSI index of business sentiment in large industrial companies in Japan (the leading indicator of Tankan) for the third quarter showed an increase from -2.9 to 9.4 with more modest expectations of 4.8. Producer prices in August rose from 2.6% YoY to 2.9% YoY versus the slightly higher forecast at 3.0% YoY. The US stock index S&P 500 also added 0.08% yesterday, while Dow Jones is preparing again to establish a new historic record of 0.18%. Moreover, Asian stock indices currently trading mixed, as the confusion was caused by the flop data from China. Chinese Industrial production fell from 6.4% YoY to 6.0% YoY in July against expectations of growth to 6.6% YoY. Retail sales for the same month fell from 10.4% YoY to 10.1% YoY, with the expectation of growth to 10.5% YoY, and investment volume shrank to 7.8% YoY from 8.3% YoY. The index of China A50 lose 0.41%, but Nikkei 225 increased by 0.02%.

Today, the Japanese industrial production showed a downturn which was already expected and the final estimate of the July measurement was published and resulted -0.8%. The capacity utilization factor decreased by 1.8%.

Further growth is anticipated for the pair towards 111.70 considering the strengthening of the dollar in general and the growth of the stock market.