English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

EUR/USD, GBP/USD

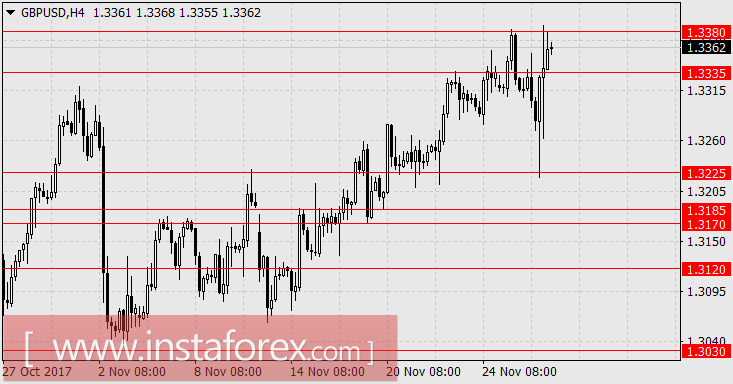

According to the results of the stress tests of British banks published yesterday, it became apparent that no credit institution is in need of additional reserve capital. All banks have passed stress tests and this surprised many investors. However, the beginning of the economic crisis is a matter of an uncertain future, and the difficulties in the negotiation process with the EU are only intensifying. This time, a problem surfaced through a deal on the border of Ireland with Northern Ireland - a coalition agreement between the parties Fine Gael and Fianna Fail was broken. Thus, the unresolved major issue on the border practically halted the entire negotiating process. This situation persisted until the evening, during this time the pound fell by 100 points. However, in the evening, news emerged about the resignation of the vice-premier of Ireland, Francis Fitzgerald, thus removing the primary threat of parliamentary re-elections. It also became known that the approximate amount of British compensation for withdrawing from the EU - 45-55 billion pounds - was determined, which investors considered good news, as the EU no longer insists on 60 billion. The pound turned sharply and closed the day by a growth of 23 points.

Economic data on the US came out mixed, but with an optimistic mood it could appear good: the trade balance for October amounted to -68.3 billion dollars against the forecast of -65.0 billion, wholesale stocks decreased by 0.4% against the forecast of an increase by 0.5%. However, the index of business activity in the manufacturing sector of Richmond for November increased from 12 to 30 (forecast 14), the index of house prices S&P/Case-Shiller in the 20 largest cities in September increased from 5.8% y/y to 6.2 % y/y with a forecast of 6.0% y/y, consumer confidence in the evaluation of the Conference Board in the current month increased from 126.2 to 129.5. The common background for the strengthening of the dollar was the speech of Jerome Powell in the Senate, published a few hours earlier, in which it was said that all conditions were ready for the December rate hike.

Today, the British pound may experience a new blow, this time from the indicators of credit activity of the population. The number of issued mortgage lending permits in October is expected to be 65,000 against 66,000 in September, the net volume of new loans to individuals is expected to reach 4.3 billion pounds from 5.5 billion the previous month. At 13:00 London time, Mark Carney will speak on the event of the anniversary of the creation of the Council for Fair and Effective Markets. Presumably, about the discussion of rates and how it will be affected, in line with the current tightening of their increase. The border issue in negotiations with the EU has not been lifted - Britain was ordered to give a decision on this issue before December 4.

The US will publish the 2nd GDP estimate for the third quarter - a forecast of 3.3% versus 3.0% in the 1st estimate. At 12:30 London time, the head of the Federal Reserve Bank of New York, William Dudley, will speak on current economic issues. At 14:00 London time, Janet Yellen's speech will begin in the Congress on the subject of economic prospects. All these events, like the previous speeches of these policymakers, are likely to be directed towards a moderate tightening of the monetary policy.

As a result, we are waiting for the euro in the range of 1.1670-1.1715, the pound sterling at 1.3030.

USD/JPY

On Tuesday, US stock indices showed sharp growth, thereby supporting the yen in a critical situation - the quotation returned to the upper limit of the range of 111.00/60. The Dow Jones index added 1.09%, S&P 500 rose 0.98%, Russell 2000 gained 1.59%. All indices set new record highs. Today, the Japanese Nikkei 225 is growing by 0.32%, but the Chinese stock market continues to fall - Shanghai Composite -0.59%, China A50 -0.76%. The volume of retail sales in Japan in the October estimate fell to -0.2% y/y against 2.3% y/y in September.

Thursday might be optimistic for the industrial production data for October, the forecast is 1.9% after -1.0% the previous month. On Friday, household spending may show another decline - the monthly forecast is -1.4%, at an annualized rate of -0.4% y/y. Furthermore, the longer the Chinese stock market goes down, the more difficult it is for the yen to follow the growth of the US market. Under favorable circumstances, the yen may rise to 112.50. Growth is associated with a constant risk of falling towards 109.60. The focus of attention is shifted to the Chinese stock market.