English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The results of the May meeting of the Fed were not very bright: the US currency did not receive additional momentum for its growth and bulls of the dollar had to retreat throughout the market. The probability of a fourfold increase in the rate has again fallen, despite the general optimistic mood of the regulator. In addition, members of the Federal Reserve elected a sufficiently "diplomatic" tone for the accompanying statement, while voicing very unexpected signals.

The main message of yesterday's meeting is that further inflation growth will not be an argument for tightening monetary policy. This scenario, of course, is not ruled out, but now, it is impossible to put the "equal" sign between the growth of inflation indicators and the acceleration of the pacing of rate increase. The market obviously did not expect such rhetoric, especially on the background of the latest releases of inflation indicators.

It is important to note that the Core Consumption Consumption Index (Core PCE Price Index), preferred by the Fed,once again showed positive dynamics for the month of April with an increase of 0.2% in monthly terms and 1.9% in annual terms. The bulls of the dollar were inspired by this trend as this circumstance increased the chances of a fourfold increase in the rate this year. However, the regulator, figuratively speaking, updated the "rules of the game": the Central Bank intends to adhere to the basic scenario of raising rates. This will happen in the event that inflation will be somewhat under delivered to the target level, even if this figure exceeds the two-percent mark.

This suggests that the Fed's monetary policy continues to be an incentive rather than a deterrent. The regulator is quite calm about the possible (and very likely) excess of the target inflationary level. This fact will not become a signal to action, contrary to the desire of many market participants. In fact, the members of the Federal Reserve broke the habitual cause-and-effect relationship, somewhat disorienting the market.

In addition, the Fed was not unambiguously optimistic about assessing the economic situation. In particular, he pointed to a slowdown in the growth of consumer spending on the background of steady growth in the fourth quarter of last year, as well as against the background of an increase in the volume of business investment in fixed assets.

However, this remark is not so important in comparison with the main aspect of yesterday's meeting. The American regulator emphasized in a separate line that when considering the prospects of monetary policy, he will be guided not only by the labor market but also by inflation. From the accompanying statement, it was even ruled out that "the Fed closely monitors inflation rates." The Fed expanded the range of analyzed information, including indicators of labor market conditions, indicators of inflationary pressures, and inflation expectations and data on "changing financial and international conditions."

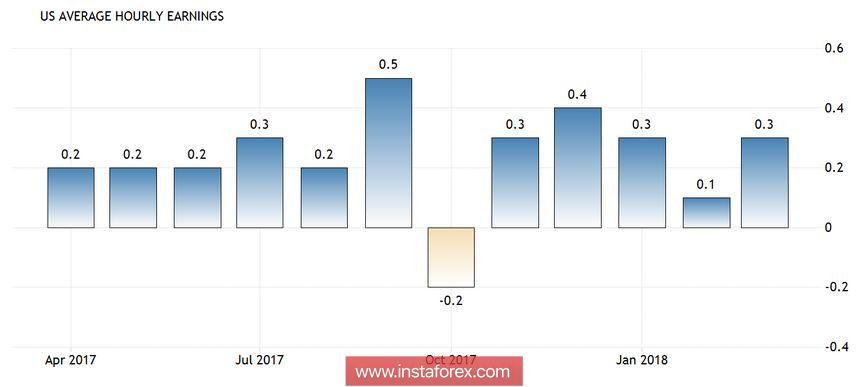

In other words, the growth of the Core PCE indicator is not an end in itself but a necessary condition. This in turn should be consistent with other fundamental factors. Such, for example, as an increase in the average hourly wage. This indicator has been fluctuating in the range of 0.1% -0.3% (monthly terms) since November of the previous year and 2.5% -2.7% in annual terms. The head of the Fed, Jerome Powell, has repeatedly said that this is an extremely weak increase in wages with such a strong strengthening of the labor market. It is likely that now, the Fed will focus its attention on this indicator, which, contrary to all arguments, remains below the desired level. That is why tomorrow's non farms can provoke quite a strong volatility throughout the market, and above all for the EUR/USD pair.

Most analysts traditionally expect the further strengthening of the US labor market. Once again, analysts predict a reduction in unemployment to 4% (although this forecast is not justified for two months in a row), as well as an increase in the number of people employed in the non-agricultural sector to 185 thousand. The ADP report, which was published yesterday, confirms the validity of these forecasts. According to the experts of this agency, 205,000 jobs were created in the USA for the month of April.

However, recently, non farms influence the market only in case of a significant deviation from the forecast values. The main attention of traders is focused on the indicator of wage growth. According to general expectations, this indicator will again slightly decrease on a monthly basis (to 0.2%), remaining at the same level (2.7%) in annual terms.

Obviously, if this forecast, which is already very weak, does not justify itself, and the growth of wages will slow down, the dollar will lose one more point of support. In addition, we got the impression that the market has not yet fully realized the significance of yesterday's changes. It is likely that most traders decided to wait for the June meeting to hear the position of the regulator and other relevant comments straight from the mouth of Jerome Powell. This explains the stalemate that we are witnessing today: the dollar rally has stopped, but no one is able to get rid of the greenback either. Friday non farms can push traders to one of the solutions: either to stay true to the trend, or to fix profits.