English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

ExxonMobil is an integrated oil and gas company that is engaged in the exploration, production and processing of oil around the world. It is the world's largest processor and one of the world's largest producers of commercial and specialty chemicals.

Its net income for the fourth quarter of 2019 was $ 5.69 billion, as compared to its $ 6 billion of the previous year's quarter. The total dividend yield for 12 months is 5.74%, while the forward dividend yield is 5.74% as well.

On February 10, Chairman and Chief Executive Darren Woods bought 2,858 shares at $ 59.86. Since then, the share price has increased by 1.32%.

Now, XOM's market capitalization has shrunk, as technology stocks have taken over the world.

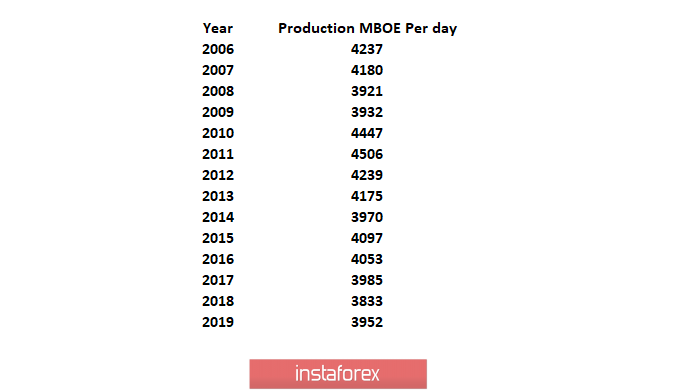

XOM did not grow, as since 2006, around the time when its share price was unchanged, its production, expressed in thousands of barrels of oil equivalent per day (MBOE), has actually declined.

This is an incredibly long period of time, and it removes any doubts on temporary problems. For both oil and gas, global production has increased during this time. At the same time, XOM sold and bought assets during this time period, as well as invested very large amounts of capital in its projects.

By investing $ 25 billion a year, it is impossible to keep production unchanged, and it is obvious that there will be problems.

The jump in 2019 was quite noticeable. Although operating cash flow was about $ 30 billion, capital investment absorbed almost all of it. Moreover, the $ 14.7 billion dividend was funded primarily by asset sales and increased debt. The current period looks much worse than XOM prices in 2019.

Based on XOM's $ 30 billion capital investment plans, operating cash flows will only be reduced to capital expenditures in 2020. There should be no dividends.

Because of this, we can assume another odd increase of $ 15 billion in debt over the course of 2020. XOM will need an excess of $ 75 WTI in band price, as well as an excess of $ 3 in natural gas in order to sustainably finance the dividends and capex.

For now, the company will increase its debt to finance its dividends and capex (provided that the natural gas prices remain at the same level).

A more likely situation is that XOM will have to either cut its expenses, or pay the dividends. Targeting smaller projects with higher returns will help improve the balance between supply and demand, as well as stop the subsidization of global energy costs at the expense of shareholders.

You can evaluate energy prices positively, but XOM's capex and dividends simply do not allow to do this.

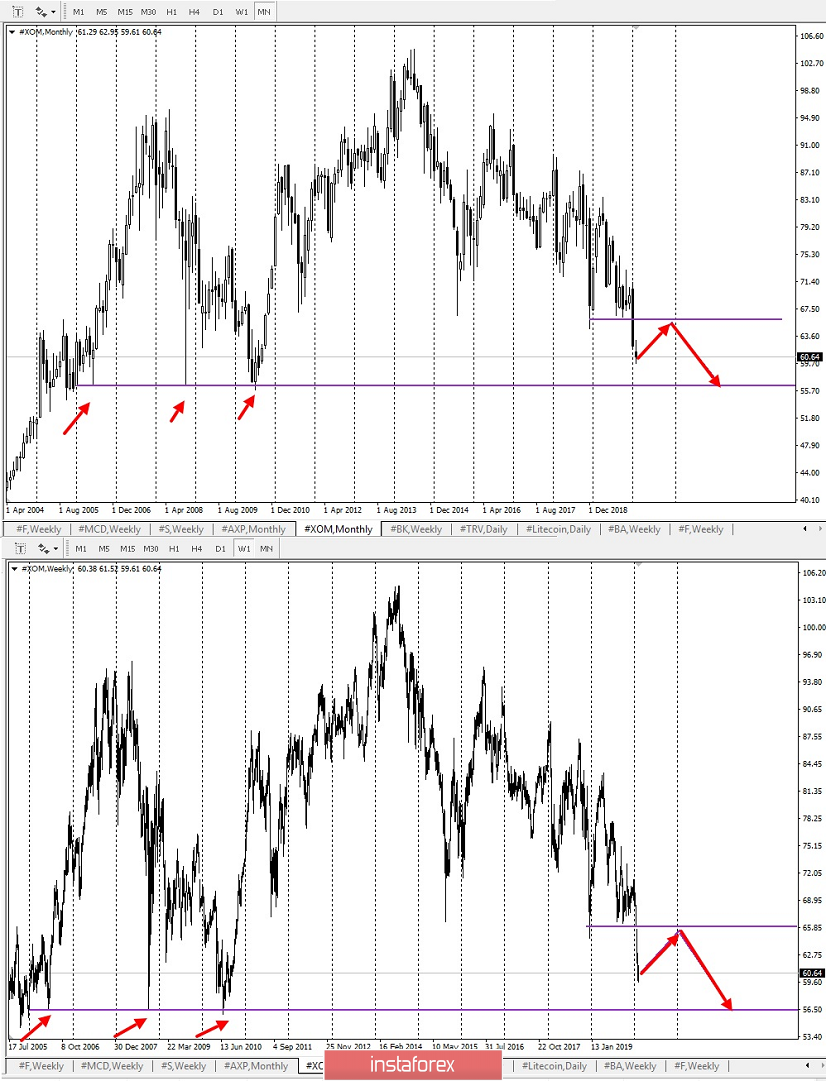

XOM problems are a sign of volatile commodity prices. The company can either accept this reality, or continue to dig itself a hole and promise a profit of "up to $ 35 per barrel." The correct approach is to return capital investments to where there is a steady return on invested capital. For this period though, it can be assumed that all the capital will be wasted. Perhaps, this may lead to a change in the company CEO. Ultimately, prices must rise to reflect what energy companies need to make money. It would be foolish to bet against XOM when the mood is so one-sided, so we should take a neutral point of view. However, based on a technical analysis, at the moment, there is no major increase expected on the company shares.

We recommend working on short positions, with a pullback to the technical levels shown on the chart.

Good luck in trading and control your risks!