English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Not temporary: inflation is going to linger

Analysts were likely over-optimistic about their predictions of the extent of the Covid-19 pandemic damage. Autumn has come, and most countries report on new records of coronavirus cases: the virus is more resistant due to less daylight hours and continues to spread around the world.

Consequently, lockdown measures disrupt supply chains and affect the business profit and ultimately the GDP of some countries. Chinese pandemic measures are extremely severe. Tight restrictions prevent new outbreaks expeditiously. However, they also cause shipment delays at ports, and importers have to await goods delivery.

Importers are forced to overpay for commodities due to delays as the world's prices are hitting all-time highs. European natural gas went up 25% in half a month. Besides, oil has climbed $80 a barrel for the first time since 2014. Fertilizers hit a record high on Friday, indicating that food prices (already hitting 10-year high) are likely to rise even higher.

Food price growth is likely not so strongly to affect the temperate zone, where the crop has already been planted. However, countries with planting crops several times a year, as well as greenhouse farms will have to cut their expenses. Moreover, farmers often take out loans against a future harvest.

The service sector is really growing, though it is not always caused by positive developments.

Briefly, this is an outline of the global economy today.

Consequently, the world's central banks are becoming increasingly concerned about rising inflation.

Sometimes it is hard to interpret the effect of tighter monetary policy on broken supply chains or energy shortages. However, it is not aimed to improve the economic situation.

In fact, central banks have just depleted their reserves. It is not possible to maintain a further dovish policy for the majority of states. Moreover, it is necessary to borrow money to keep providing loans to banks and businesses. It is carried out by means of government and corporate bonds. Consequently, the national debt is growing. Besides, at the time when interest payments are due, the government may have difficulty paying off all the contracts and government bonds immediately.

Accordingly, it is too early to discuss economies operating out of pandemic mode, although there are constant media reports about the end of the COVID-19 crisis and the global economic recovery.

The fact is that in case a particular country, for example the UK, announces that lockdown measures have been lifted, there are still severe economic restrictions in other countries and they cannot operate properly under contracts with England. Besides, the most significant among them is the Chinese economy.

However, these aspects are not an obstacle for investment managers to plan higher yields when buying bonds. It is easy to understand: they are obliged to provide their clients, who are investors, with a higher yield to cover the inflation rate. Besides, they intend to make some profit, though it is very difficult to do in a period of stagflation. Consequently, they often use risky assets with high yields like cryptocurrencies. This is one of the reasons why bitcoin is strongly supported during sell-offs.

Moreover, stagflation has been familiar to everybody for the past two weeks. Unemployment rate is too high. Besides, prices and inflation are rising. Therefore, in contrast to optimistic analysts' forecasts, there are rather pessimistic scenarios in the near future.

Besides, reasons for rising prices ranging from delivery delays to a surge in demand after the blockage are similar to the one-time effect of the COVID-19 pandemic. Accordingly, the prevailing view used to be that any surge in inflation would not last long.

For example, the International Monetary Fund recently reiterated its promise that inflation will normalize as soon as early 2022. According to the IMF forecast, annual inflation in advanced economies will hit record highs at an average of 3.6% in the final months of this year and regain to 2% in the first half of 2022, in line with central bank targets. The IMF added that emerging markets would demonstrate faster growth, averaging up to 6.8% and then declining to 4%.

This scenario is possible, if the coronavirus pandemic eases. As long as the trend is reversed, it is rather irresponsible to state that the targets have been reached. However, the IMF aims to prevent a panic among the population. Besides, it may immediately result in a greater shortage of certain product categories and increase price pressure, as happened recently in Britain due to fuel shortage.

However, this position is now being actively reconsidered.

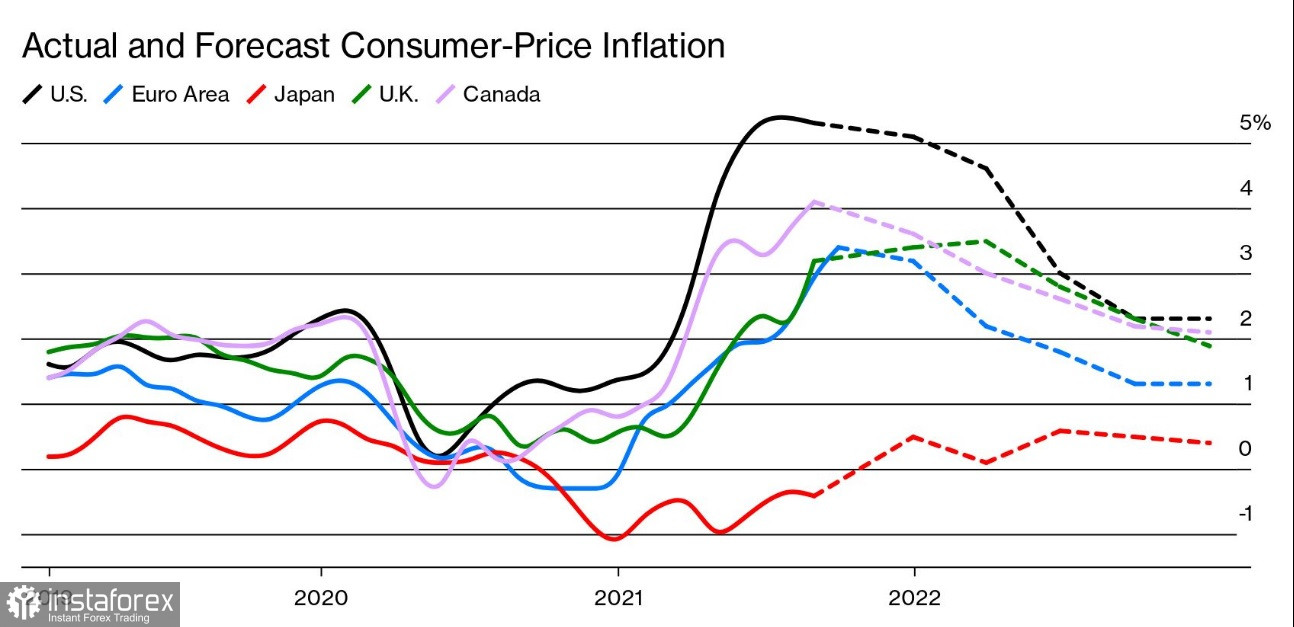

Inflation is likely to last long

Last week, Hugh Pill, the Bank of England's new chief economist, openly admitted that the extent and duration of the transitional surge in inflation was greater than had been expected.

The pandemic situation has not been curbed, which means businesses as well as supplies remain under attack.

Even when the coronavirus pandemic does end, there may still be consequences ranging from households with excess savings to shortages of certain categories of workers. Besides, these distortions have the potential to keep inflation high. Moreover, a spike in energy prices would increase the cost of many other products.

It is still difficult to predict the long-term effects of the COVID-19 crisis on the financial position of some states. In any case, growth is bound to start. However, traders and investors are concerned about the delay.

Notably, the cost of living is not rising everywhere.

Inflation in Japan is negative. However, in other Asian countries it is still low. Besides, there are strong factors ranging from trade to employers' inability to surge prices that have held prices down before the coronavirus pandemic since 2009. These factors may become more determining when the COVID-19 crisis ends. Moreover, their impact is likely to be amplified many times over by rising government debt for almost every sovereign.

Philip Lane, chief economist at the ECB, stated that the red zone was intended if inflation became stable at levels that were excessively above the inflation target. He noted that it was too far from the eurozone. However, in case inflation becomes extremely high, it will be too late to take measures.

Philip Lane added that they had to share the opposite views, meaning that ECB experts should support the bank's official position and consider only the positive scenario.

Bank of Canada Governor Tiff Macklem said that the situation proved to be more complicated. He highlighted that there was some risk that the price pressure would be higher than they had expected. However, as the regulator supporter he added that there were good reasons to believe it was temporary.

Reasons for further inflation rise

Supply rates...

During the COVID-19 pandemic, the structure of demand has changed considerably. For example, instead of air travel, customers prefer to own their car, providing isolation unattainable with public transportation. Instead of traveling abroad, biking has become popular, allowing people to spend time with health benefits and keep distance.

The changing structure of demand is exerting enormous pressure on the world's ability to produce and transport goods.

Growing interest in cryptocurrencies is creating new centers for mining them. At the same time, the demand for electric cars is growing worldwide, not least due to fuel prices. This forces miners to compete with automakers for the microchips used by both industries. Besides, the more traders invest in tokens, the greater interest in producing them. As a result, demand is rising.

For example, on Monday IHS Markit cut its forecast for global auto production by more than 9% in 2022, indicating a shortage of semiconductors.

Vietnamese factories that make shoes and clothing for the world are facing a staff shortage as migrant workers prefer to wait out the pandemic in their home provinces.

There are many such examples of the changed structure of demand.

Today, demand is still skewed toward commodities. However, local virus outbreaks, shortages of raw materials and other resources, such as summer disruptions in nickel mining, or the threat of losing Guinea as a source of aluminum, as well as irregular energy supplies continue to reduce supply.

The pandemic shortage situation eventually forces many governments and companies to rethink their dependence on foreign suppliers and to be more frugal with raw materials. The European Union, for example, plans to produce more semiconductors domestically.

However, using local resources and storing more commodities may increase costs. This would require such measures as subsidies, corporate bonds, or taxes on imports. This could prevent inflation from normalization.

Are households saving?

The majority of the population in many countries is limited in contact and, in fact, they are "stuck" at home. Policymakers believe that it has allowed citizens to accumulate some reserves that are now not being used.

For example, according to the Federal Reserve, Americans had accumulated about $2.5 trillion in excess savings by June. Europeans have accumulated 540 billion euros.

Economists think this strategic reserve may support consumer spending even as prices rise.

However, the situation is complicated. The lion's share of these savings is actually in banks, at least in the US and eurozone.

This means that this money is already being used right now for lending and other banking operations. Consequently, it is not excluded from circulation.

Besides, inflation absorbs some of this money as low interest rates set by the government keep interest rates on deposits low.

Moreover, if even some households consider these savings as an opportunity for investment, such as Forex trading, or cryptocurrency trading, then the consumption capacity of these households falls.

Besides, there is also a problem with the distribution of these savings. As usual, the upper middle class was able to save the most. It is common that these people are more inclined to invest. After the pandemic is over, they will certainly fly on vacation. However, this spending will make up only a small part of their investment. Moreover, the upper middle class is now wasting money on fun activities like buying their own boat and other things that allow them to relax without breaking the lockdown restrictions.

As for the poor, they are likely to have spent unemployment benefits and other subsidies on roof repairs ahead of the next winter and similar services. Consequently, their savings are not that great.

As for developing countries, there is usually no way to save some amounts.

Hence, hopes for reflationary trading are not fulfilled as almost all the money saved right now revolves around financial markets in instruments like forex trading or bitcoin futures.

The report to the European Parliament highlighted this problem at least partly. However, it may explain a reason why inflation will be more serious than experts had expected.

Employment and employed...

Wages have grown slowly over the past decade. Manufacturers, bound by competitive prices, could not increase their wage fund too much. However, the situation is changing.

Unemployment remains higher than it was before the pandemic. Usually this factor negatively affects the level of wages. However, not at the moment.

Vacancy rates are also at record highs in almost all countries. It gives workers in some industries more chances during job interviews. They have a right to insist on wage increase if inflation is extremely high.

However, rising wages may set a spiral of self-inflation. In this case it will be difficult to curb.

Notably, demography may also lead to a long-term shift in favor of labor in developed countries. Reduction in the working-age population would result in higher wages and possibly higher inflation.

Besides, globalization will not benefit, as it did at the end of the last century, when the stores were piled with goods from China, Eastern Europe, and other developing countries. This cycle is coming to an end as companies have no new low-cost workers pool.

However, we should note the changing market structure of employment. During the COVID-19 pandemic, remote work has developed at a rapid pace. Many skilled workers from developing countries took the positions of higher-paid local citizens.This trend will continue to grow, giving employers more freedom.

There are other arguments in favor of rapid falling prices.

Arguments for temporary inflation

Many analysts are predicting a return to traditional inflation rates as the coronavirus crisis eases.

Economist Dario Perkins believes that consumers will replace 'experiences' with 'things,' reducing the pressure on global industry. He states that commodity price flexibility, the source of inflation in 2021, should be the source of disinflation.

Sharpening supply chains is likely to reduce manufacturers' hectic demand, and hence final prices.

Meanwhile, there's another factor that decreases manufacturers' demand, indicating too high prices. A number of industries, such as the jewelry industry, may suffer from insufficient demand from buyers even if supplies improve.

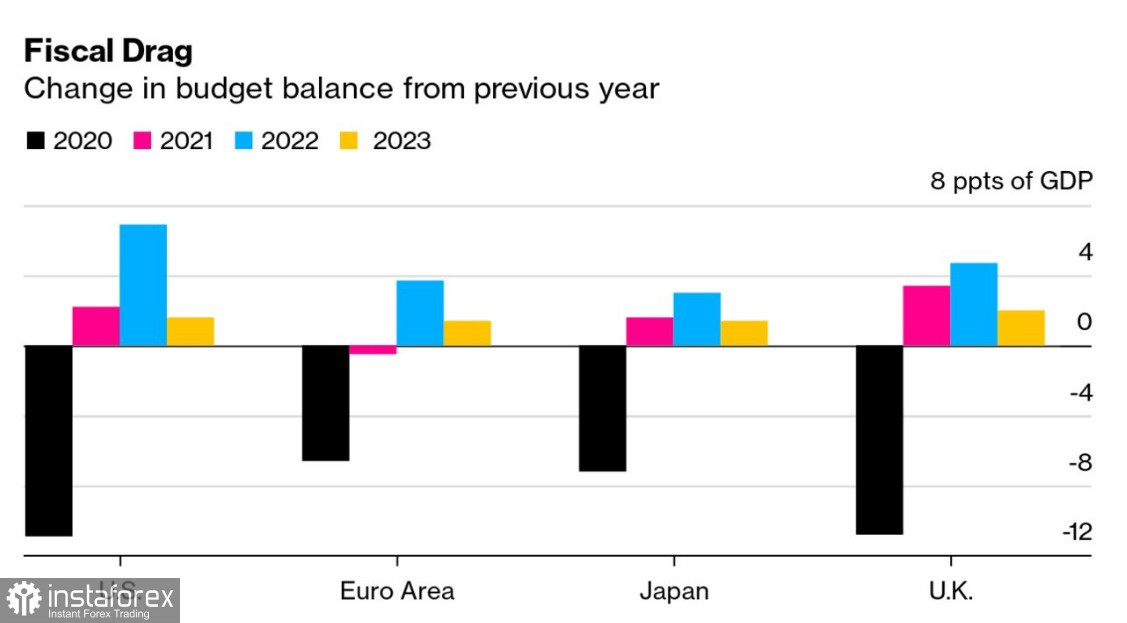

Stimulus makes history

Government spending backed the economy. However, if interest rates keep low, fiscal policy will inhibit rather than promote economic growth.

Over the past couple of decades, import policies in the developed world have focused on austerity. This is likely to remain the case.

In the US President Joe Biden's Democrats are cutting their spending plans. Europe may adjust its budget constraints before restoring them.

Besides, there is not enough political momentum to completely abandon them. Moreover, using semiconductors as an example, we may observe how the changing structure of demand affects imports as the flow of imported goods simply shifts. If not oil, then semiconductors. Imports remain high; their segments change.

Consequently, it doesn't matter whether the final products or components are imported, there is still demand for international supplies. Besides, it is growing due to the consumer environment. Europe can produce semiconductors, however it cannot create a second Samsung or Iphone with a distinct competitive advantage in the short term. Moreover, high prices for gas and other consumables result in high prices for European goods, although China could lose its investment appeal as well.

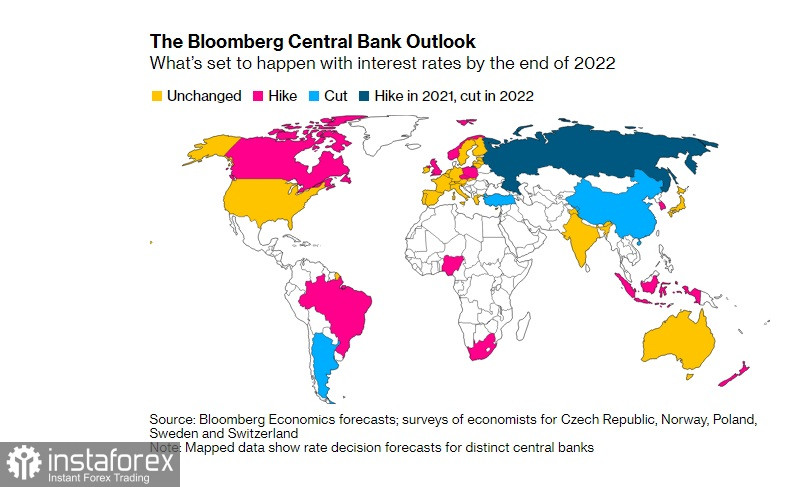

Meanwhile, central banks, which currently have limited capacity to accelerate the economy, remain in a wait-and-see mode. Interest rates could be raised moderately so as not to hurt the major banks.

Besides, low rates are temporary, even if regulators are now inclined to face slightly higher inflation. The anticipation of this event is one reason investors have been willing to accept the price spike throughout the year.

Some countries are already tightening the credit terms, including New Zealand and Norway, which are raising interest rates. The Fed is preparing to slow its asset purchase program.

Outcomes

Fed Chairman Jerome Powell declared Congress in early 2021 that the long-term dynamics of inflation were hardly changing. He was referring to the long-term forces that have kept inflation low.

For example, wages are still unable to show a significant increase outside of the pandemic as employers simply cannot pay more amid competition with Asian manufacturers. Globalized trade, which has made goods cheaper, is stable due to rising prices and in the online segment as well. Technological breakthroughs are accelerating, and many of them are cutting costs.

More than a decade before the pandemic, the deflationary trap looked more dangerous for developed countries than skyrocketing prices.

When the COVID-19 crisis ends, these factors may still be relevant only if it causes no serious damage due to the pandemic spread. If the coming winter is too hard for manufacturers and the public in terms of prices, there is a good chance that businesses will begin to close, unable to withstand loan repayments and reduced demand. Indebtedness of the population and the industrial population to the banks will not allow the financial institutions to cover the interest on loans by themselves. In this case the risk of a Great Depression scenario will increase many times. Consequently, the exhaustion of the financial system and its extent really matters.

We observe the first signs of bankrupt Archegos and nearly bankrupt much larger crediting bank Evergrande.

These considerations make investors to fluctuate wildly in sentiment, with the S&P 500 Financial Institutions Index fluctuating in a wide corridor all last week.

Fluctuations in the S&P 500 index exceeded 1% for six consecutive sessions until Thursday, the longest period of volatility in six months.

Overall, this process is a vivid reflection of investors' thinking about the current situation. The uncertain sentiment is making the market nervous. The index has been steadily declining since the beginning of September, although this is partly due to the traditionally difficult months for the financial industry.

On Friday, weak US labor market data were the reason for the index and most stocks in all segments dropping. However, as the US trading started on Monday, the chart rose again. At 1:44 pm GMT, the index had added about 16 points due to a rebound in the oil market. However, the bears further consolidated, and at 6:00 pm GMT, with oil up, the S&P 500 index was down 12.79 points.

After more than a year of no results, short traders just had their fifth consecutive week of positive returns. This is the best result since 2018. In another case that was problematic in the past, individual stocks have begun to move in unison, which is an alarming sign.

However, bulls are retreating due to growing uncertainty.

The percentage of newsletter writers categorized as bullish in the Investors Intelligence survey fell to 40.4% this week, the lowest since March 2020, according to data compiled by Yardeni Research. However, the percentage of supporters of a market correction jumped to 37.1%, the highest in the same period.

Besides, until there are low interest rates, the market will be inclined to buy as there is cash and it is obligatory to invest it. Consequently, the near-term outlook promises growth. It is hard to predict what will happen after the rate hike. Especially, if there is a delay.

However, the banks are already lowering their growth rate forecasts. For example, Goldman Sachs revised figures of the previous forecast, reducing the expected performance to 4% per year. The company lowered its previous forecast in late July. Despite the optimistic rhetoric of the company's representatives, the figures convince that prime brokers do not expect a full recovery of the industry next year. This means something.