English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

*) see also: InstaForex Trading Indicators for NASDAQ 100 (NDX)

The US equity market is recovering after a period of elevated volatility driven by geopolitical and trade risks. Key indices, including the NASDAQ 100, the S&P 500, and the Dow Jones, moved higher as tensions between the US and the European Union eased and fears of a widening trade conflict receded. The NASDAQ 100, which reflects the performance of the largest US tech companies, was among the leaders of the recovery, with futures (NDX on the trading platrom) up about 0.75% to around 25,600.0 at the start of Thursday's US session, underscoring continued investor interest in the tech sector despite lingering risks.

This move was a reaction to a combination of key factors: a reduction in geopolitical threats and stronger US macroeconomic data.

Main growth drivers

Geopolitical de-escalation acts as the primary catalyst. Markets breathed a sigh of relief after President Donald Trump said he was abandoning threats to impose 10% tariffs on goods from eight European countries and was pausing plans related to Greenland. News of a "framework for a future deal" with NATO sharply lowered immediate risks of a full-scale trade war, which had been viewed as a major threat to global growth and corporate profits.

Strong macro data. On Thursday, data confirmed the resilience of the US economy:

- Revised Q3 2025 GDP rose to 4.4% year-on-year, exceeding initial estimates and market expectations (4.3%). Growth was driven by higher exports and investment.

- The labour market remains resilient. Despite a small increase in weekly initial jobless claims to 200,000, the 4-week moving average declined and continuing claims fell to 1.849 million, indicating stability.

Dollar weakness. The US dollar index (USDX) fell to 98.55, which is positive for revenues of US multinationals, particularly in the tech sector, a large share of whose revenues are generated overseas.

Focus on NASDAQ 100: tech sector under scrutiny

The NASDAQ 100's rise reflects a broader increase in risk appetite, but the sector faces its own specific agenda:

- Corporate reports. The market awaits results from tech giant Intel, as well as Procter & Gamble and GE Aerospace. Results and, more importantly, companies' forward guidance will be a key indicator for assessing corporate America's health.

- Inflation expectations. Investors' attention on Thursday will focus on the Personal Consumption Expenditures (PCE) price index, the Fed's preferred inflation gauge. This release (15:00 GMT) will shape market expectations for future monetary policy. Any signs of a sustained deceleration in inflation could support markets, while unexpectedly high prints would create pressure.

- AI investment. Despite measured optimism, investors remain cautious about the long?term profitability of AI infrastructure investments because of high capital intensity. This creates selectivity within the sector: the market will "weed out" companies without clear monetization paths and sustainable financial models.

Prospects and risk factors

In the short term, sentiment remains constructive, but the durability of the rally will depend on several factors:

- PCE inflation data. This is the day's key event. Signals of continued disinflation would strengthen hopes for eventual Fed easing and support equity valuations.

- Corporate reports. Earnings season is peaking. Weak guidance, especially in tech, could quickly cool optimism.

- Geopolitical stability. Markets have priced in de?escalation, but any return of hardline rhetoric on Greenland or other issues would be a material negative surprise.

- Fed policy. Despite strong data, the market will seek confirmation that the Fed will not tighten and will preserve the option to ease later. The January 28 meeting is the next important milestone.

Main scenario

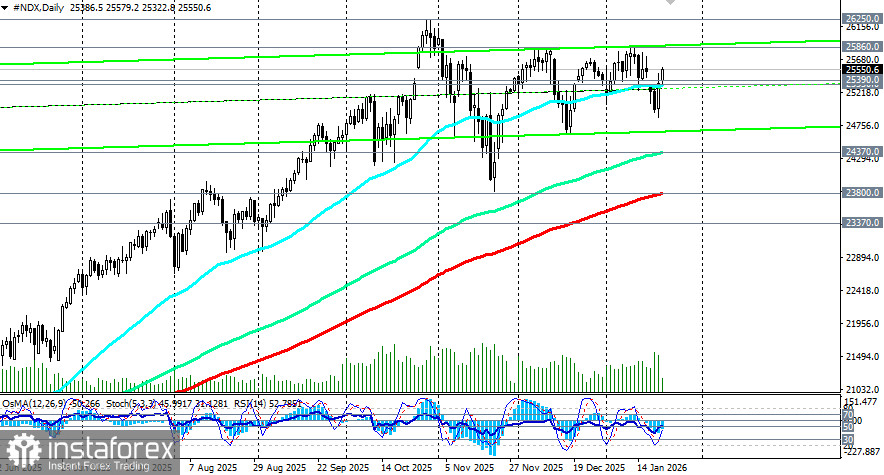

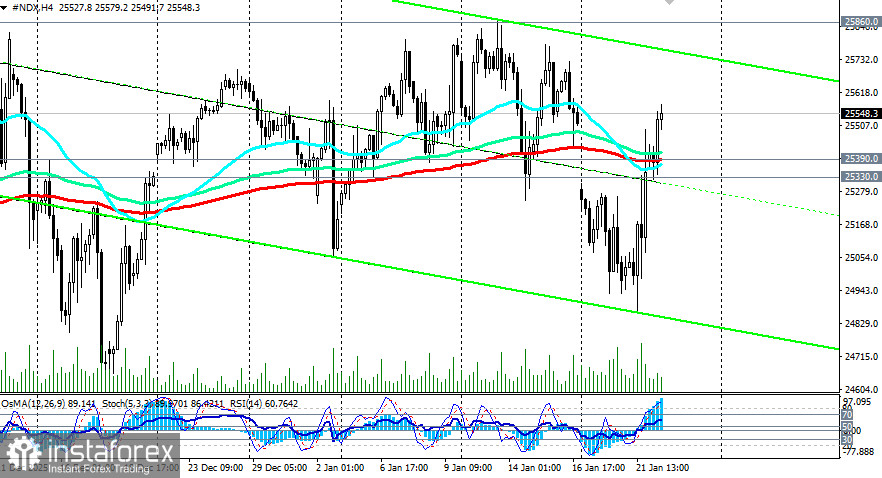

With a moderate geopolitical backdrop, stable US macro data, and neutral Fed policy, the US equity market is expected to continue to recover, and the NASDAQ 100 may trade in the 25,330.0 (EMA50 on the daily chart) – 25,860.0 range (local resistance corresponding to December/January highs).

Alternative scenario

If US trade rhetoric hardens, corporate reports disappoint, and bond yields spike, the index could correct toward 24,370.0 (EMA144 on the daily chart) – 24,400.0. A break below 25,330.0 would be the trigger.

Conclusion

The US equity market — and the tech sector in particular — is in a recovery phase supported by geopolitical de-escalation and strong macro prints. The NASDAQ 100 is posting confident gains in line with broad sentiment.

However, optimism is cautious. Investors are closely monitoring corporate earnings and inflation data to judge whether fundamentals support further upside. In the coming days, market direction will hinge on the balance between hopes for a soft landing in the US economy and concerns about future corporate profits and Fed policy. The current momentum is positive, but sustaining new highs will require fresh confirming signals.