English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

See also: InstaForex trading indicators for S&P 500

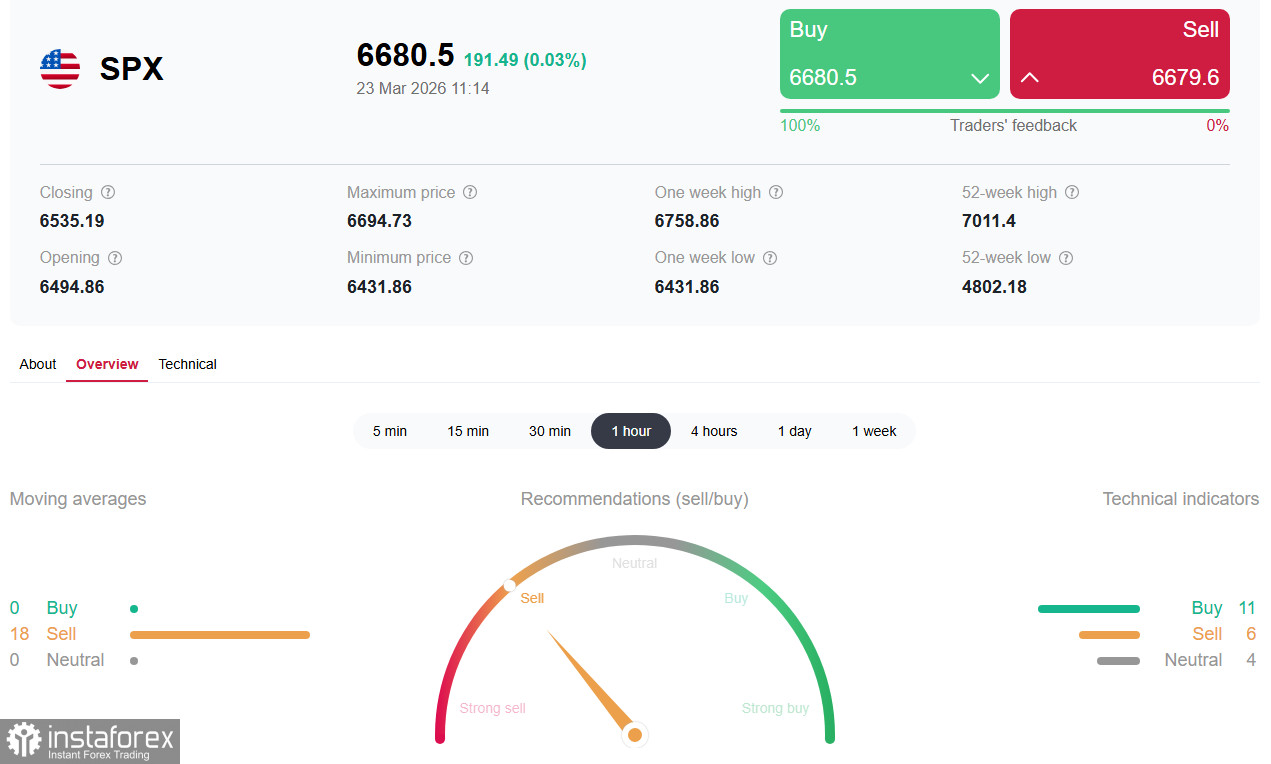

Having finished the fourth consecutive week in the red zone, the broad US market index S&P 500 continues to decline at the start of the current week, trading around 6450.00–6440.00 in the first hours of the European session. This is roughly 7% below the January record highs above 7000.00. The market has found itself at the epicenter of a perfect storm: escalation of the Middle East conflict, explosive oil price growth, and a radical revision of expectations for Federal Reserve monetary policy.

Current situation: key levels breached — oil rules roost

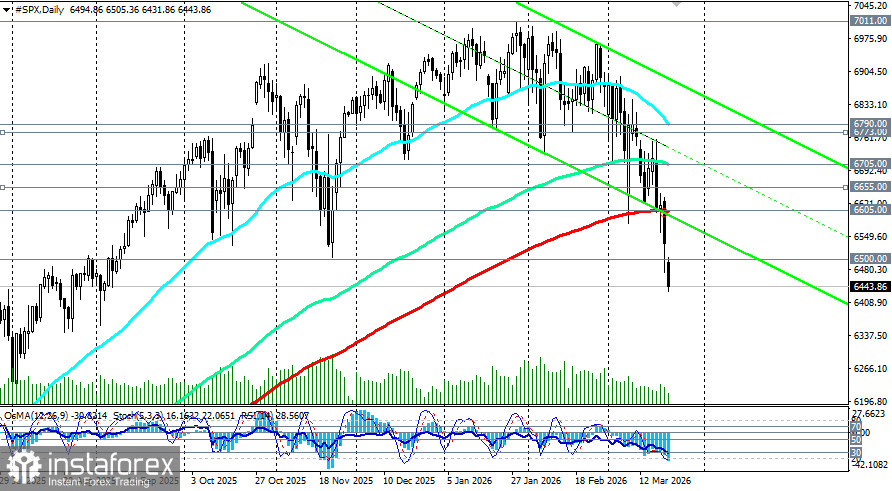

Today, the S&P 500 lost another key technical support. The index fell below the weekly 50-period exponential moving average (50-period exponential moving average) at 6500.00 for the first time since May 2025, which can be considered a warning signal. Earlier, in early March, the index broke the 6705.00 level (the 144-period exponential moving average on the daily chart) and declined toward the key support level of 6605.00 (the 200-period exponential moving average on the daily chart), which from a technical analysis perspective could have been seen as a "bear trap," behind which there was a lack of support down to 6500.00.

However, no rebound occurred, and the correlation between the S&P 500 and the oil price reached negative 0.93, indicating an almost perfectly inverse movement. The market has become hostage to an energy crisis: West Texas Intermediate oil prices exceeded one hundred dollars per barrel after Iran blocked the Strait of Hormuz, and today they remain close to that level.

Energy companies included in the index, such as Exxon Mobil and ConocoPhillips, benefit from the oil price spike. However, this sector represents less than four percent of the index's weight, which is insufficient to offset declines in other segments.

The main laggards have been the high-technology companies that dominated the market in 2025:

- Nvidia has retreated from peak valuations amid fatigue with the artificial intelligence theme.

- Microsoft has declined by more than 17% year to date amid slowing cloud revenue growth.

- Amazon has lost about 13. 5%.

Even traditional defensive sectors — consumer staples and real estate — have failed to hold ground, indicating the systemic nature of the selloff.

Key factor: Federal Reserve's hawkish reversal

Markets have experienced an unprecedented revision of expectations for monetary policy. In just a few weeks, expectations shifted from three rate cuts to the probability of unchanged policy through the end of the year. According to the CME FedWatch Tool, traders now price in an 85.5% probability of the rate remaining unchanged at the April meeting.

Federal Reserve rate futures no longer price in even one cut in 2026, and markets are beginning to consider the possibility of a rate increase. This radical change occurred in just two weeks and reflects concerns that the inflation impulse from the oil shock will prove persistent.

At the March Federal Reserve meeting, the policy rate was held in the range of 3.50–3.75%, but updated projections changed market expectations:

- The median projection for the Personal Consumption Expenditures inflation rate for 2026 was raised to 2.7% (from 2.4% in December).

- The dot plot implies only one rate cut in 2026.

- Seven members of the Federal Open Market Committee (compared with six in December) do not see rate cuts this year.

Jerome Powell acknowledged that the "oil shock" will affect inflation dynamics, although there is not yet sufficient data to assess the scale of the impact. However, markets heard the key message: without progress in lowering inflation, there will be no policy easing.

Geopolitical factor: war spreads to energy

The conflict between the United States and Israel on one side and Iran on the other has entered its fourth week, and the situation has reached a critical point. Iran has effectively blocked the Strait of Hormuz, through which about twenty percent of the world's oil and liquefied natural gas shipments pass vessel traffic fell from eighty-four to fewer than ten per day.

President Trump gave Iran forty-eight hours to reopen the strait, threatening strikes on energy infrastructure, while Washington is considering a ground operation to seize Iran's Kharg island — a major oil export hub. In response, the Islamic Revolutionary Guard Corps threatened to completely close the strait and to destroy American assets in the region.

This week attacks on energy infrastructure have intensified. Iran struck facilities in Qatar, Saudi Arabia, and the United Arab Emirates. Qatar reported the loss of seventeen percent of its liquefied natural gas production capacity, the restoration of which will take three to five years. Gasoline prices in the United States have risen by more than fifty percent since late February.

A joint statement by the United Kingdom, France, Germany, Italy, the Netherlands, and Japan confirmed their readiness to ensure safe passage through the strait, but a military solution has not yet been found.

Conclusion

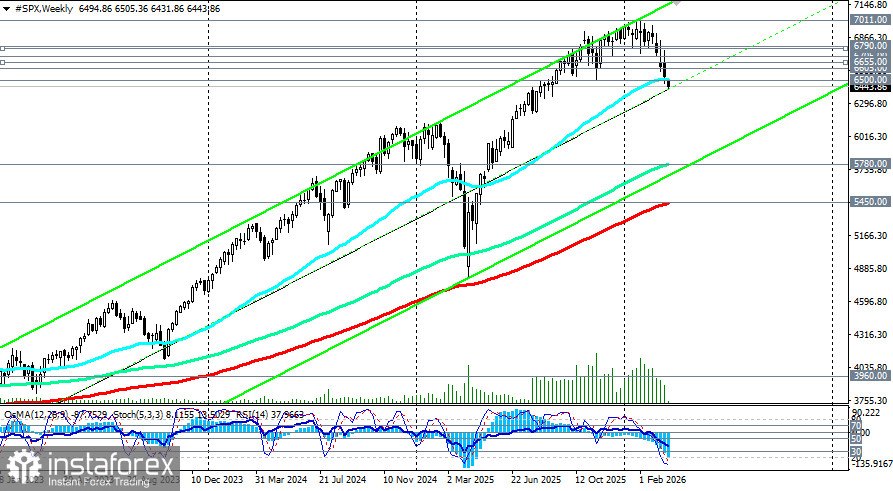

The S&P 500 is at a critical threshold. The index closed at 6535.00 at the end of last week, falling below the 200-day moving average (660.00) and the 50-week moving average (6500.00) for the first time since September.

The US equity market is undergoing a tectonic shift. Four weeks of declines, breaches of key technical levels, and a radical revision of rate expectations all point to the end of the "easy money" phase and the start of a period of heightened uncertainty.

The key zone of 6650.00–6450.00 will be decisive in the coming days. Holding above the 200-day moving average (6605.00) and a return to 6800.00 would preserve chances for recovery. A breach of 6450.00 would open the way to a deeper correction.

Investors should closely monitor developments in the Strait of Hormuz, oil prices, and, most importantly, the Federal Reserve's rhetoric regarding the interpretation of inflation risks. Under any scenario, volatility will remain high, and success will favor those who can separate short-term noise from long-term trends — structural factors (corporate earnings growth, adoption of artificial intelligence) continue to point to growth potential, but the path to new highs will be difficult and dependent on geopolitical stability and monetary policy.