English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The US labor market report for May beat expectations: 172,000 new jobs were created versus an 85,000 forecast. Data for the two previous months were revised up — from 115,000 to 179,000. The unemployment rate remained unchanged at 4.3%. Average hourly earnings rose 3.4%, in line with forecasts but below April's reading.

Markets reacted with higher Treasury yields and a notable strengthening of the dollar across most currencies. The Canadian dollar was the only notable exception, holding up thanks to an upbeat Canadian employment report.

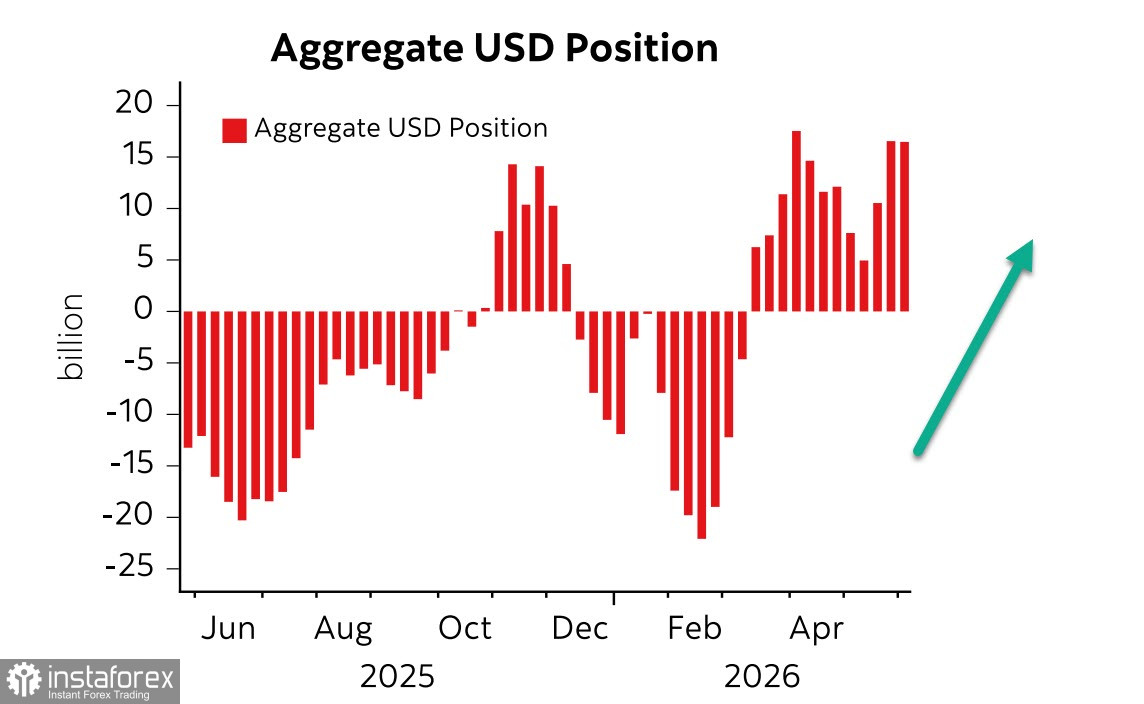

Speculative positioning in the dollar against major global currencies barely changed over the reporting week — the net bullish bias stands at +$16.5 billion, with no signs of a reversal yet.

Overall, the US economy looks stronger than expected. Despite slowdown fears, including those driven by the war, the economy shows resilience and outperforms many countries dependent on Persian Gulf developments and energy supplies. Yet a contradiction remains: although nominal GDP growth has exceeded expectations, American households are not sharing the optimism — consumer confidence is at its lowest level since early 2024, and private consumption growth slowed in Q1.

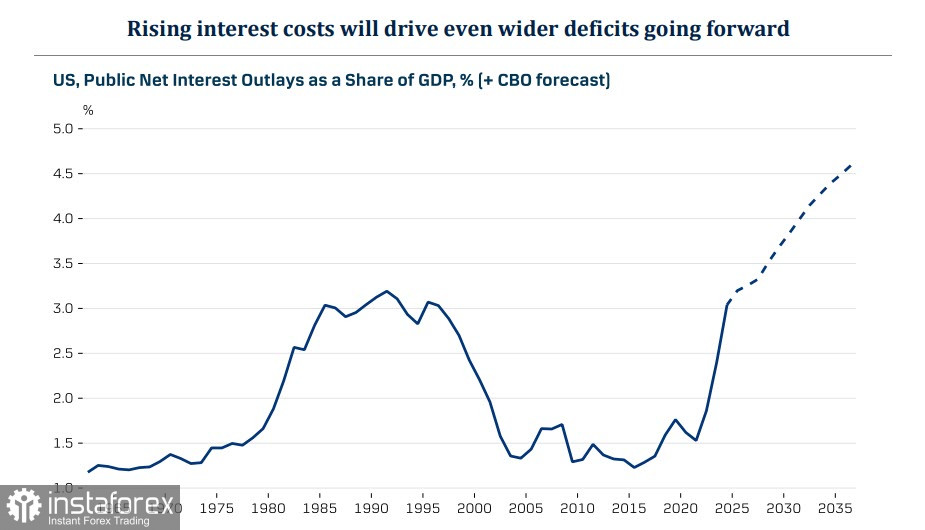

Improvements in the labor market, an ongoing investment boom in artificial intelligence, and fiscal stimulus are producing results. At the same time, longer-term risks are rising and will materialize in time, though their current impact is limited. The government is seeing lower customs?duty revenues: it is now paying out as much in refunds as it collects, which widens the budget deficit. Rapid growth of US public debt could fuel inflation if investors begin to sell Treasuries. Tighter monetary policy supports the dollar, but higher interest rates also raise government debt-servicing costs. While this is largely a medium- to long-term concern, it still undermines the resilience of the dollar?based global financial system and contributes to the process of de-dollarization.

Wednesday's May inflation report is due and is likely to affect Fed rate expectations. If inflation continues to rise — a prospect few dispute — the probability of the Fed beginning a rate-hiking cycle before year-end will increase. That scenario would provide further support to the dollar.

Political tensions in the Middle East also bolster the dollar. US attempts to force Iran into a peace deal on Washington's terms have stalled, and the confrontation between Iran and Israel intensified after renewed Israeli strikes on Lebanon.

Thus, the labor report, the revised US economic outlook, and ongoing geopolitical tensions all support dollar strength. For now, there is no basis to expect a reversal in the dollar index.