English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The EUR/USD pair remains within a local bearish impulse, but the bulls have gained some opportunities over the past week. This week, the international economic forum in Portugal featured speeches by Christine Lagarde and Kevin Warsh. In my view, Christine Lagarde adopted a more dovish and cautious tone on monetary policy, while Kevin Warsh reaffirmed the need for higher interest rates but did not clarify whether the Federal Reserve intends to reduce inflation through tighter monetary policy or expects inflation to ease naturally as energy prices decline. Since the market received no clear answer, it will have to focus on upcoming inflation data.

However, yesterday demonstrated that inflation is not the only indicator worth watching. The US labor market has begun to weaken again, and over the past three months, nonfarm payroll growth has fallen short of market expectations by more than 100,000 jobs. As a result, the slowdown in the US labor market may force the FOMC to weigh any decision on monetary tightening much more carefully. The next inflation report should give traders a better indication of whether a Fed rate hike is likely in the near future.

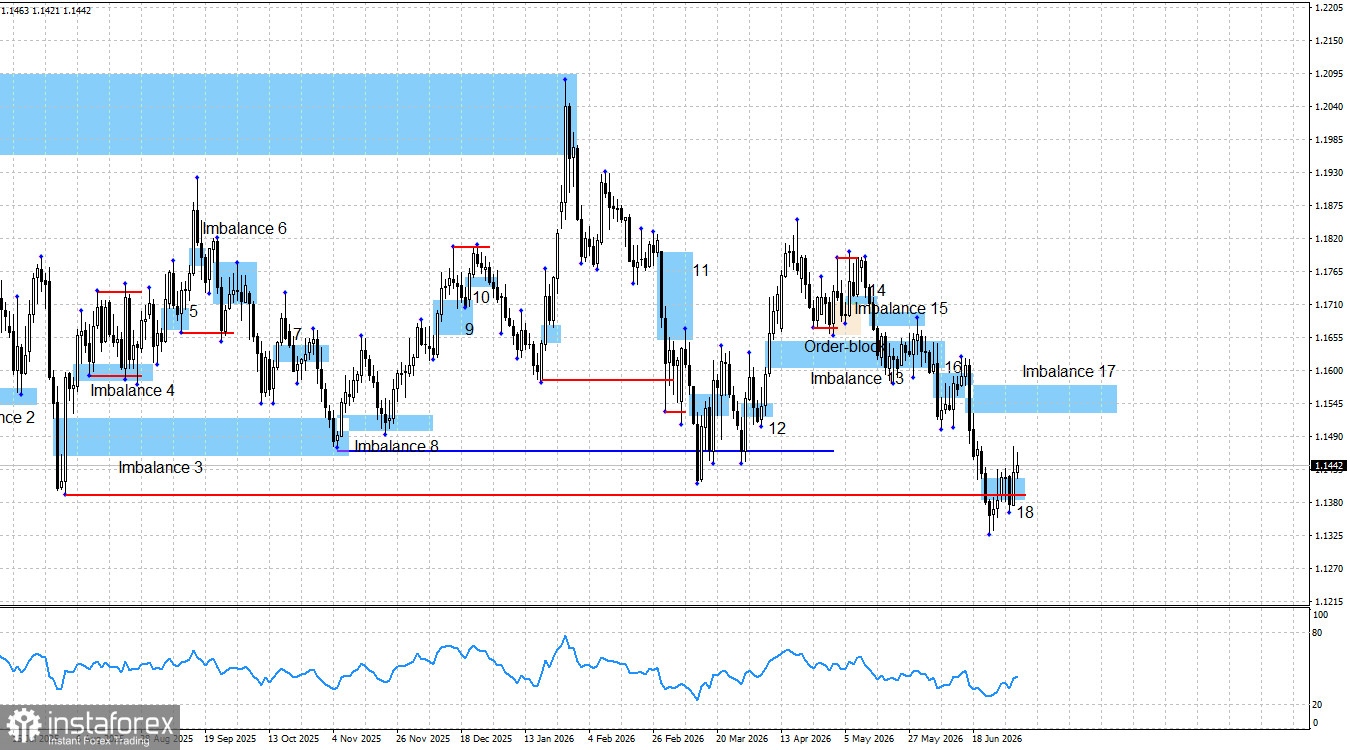

Wednesday ended with another rally in the US dollar, leading me to conclude that the market interpreted Warsh's remarks as hawkish. However, on Thursday, the dollar came under pressure following the Nonfarm Payrolls report. That bullish push was enough to invalidate bearish imbalance 18, allowing traders to shift their focus toward imbalance 17. As long as imbalance 17 remains valid, the bearish impulse remains intact. However, I would prefer to see the formation of a new bullish impulse. Either way, the bulls have been given an opportunity. The question is whether they will be able to take advantage of it.

Geopolitics has taken a back seat in recent weeks as the market focused on the Fed, but it could easily return to the forefront. Tehran and Washington have signed a memorandum of understanding, extended the ceasefire for another 60 days, and begun work toward fully reopening the Strait of Hormuz and negotiating a nuclear agreement. Despite easing geopolitical tensions, we did not see the dollar weaken as many had expected, nor did we see the euro strengthen following the ECB's monetary tightening. In fact, the opposite occurred. The bears continued to dominate despite both the fundamental and geopolitical backdrop. Now, geopolitical developments are once again disappointing the market, so renewed bearish pressure would not be surprising. Nevertheless, I do not believe the bulls' position is weak enough to justify another retreat.

The current chart structure still points to the continuation of the bearish impulse that began on April 17. Bearish imbalance 17 has not yet been fully worked off, while imbalance 18 has been invalidated by weak US labor market data. No bullish patterns have formed so far, and none are likely to appear over the next few days. Therefore, the bulls may continue a corrective advance toward imbalance 17, but there is currently no technical basis for trading that move. I would also note that liquidity may have been swept below last year's August 1 low during the past week.

There were no meaningful economic releases on Friday. Europe had no important scheduled events apart from another speech by Christine Lagarde, who had already delivered all the key messages on Wednesday. In the United States, markets were closed for the Independence Day holiday.

The bulls still have plenty of reasons to stay active in 2026, and the end of the Middle East conflict has not diminished them. Structurally and fundamentally, Trump's policies—which triggered a sharp decline in the US dollar last year—have not changed. At present, I see no significant long-term support for the dollar despite the FOMC's hawkish stance. EUR/USD has approached a series of important lows and swing points where liquidity could be swept, potentially signaling the end of the current bearish impulse.

Economic calendar for the US and the Eurozone:

- Eurozone: Retail Sales (09:00 UTC)

- United States: ISM Services PMI (14:00 UTC)

- Eurozone: ECB President Christine Lagarde speaks (16:00 UTC)

The economic calendar for July 6 contains three scheduled events, with the ISM Services PMI standing out as the most important. The economic backdrop is expected to influence market sentiment mainly during the second half of Monday's trading session.

EUR/USD forecast and trading recommendations:

In my opinion, the pair remains in the process of forming a bullish trend. The fundamental backdrop shifted sharply in favor of the bears four months ago, but the broader trend cannot yet be considered broken or complete. Therefore, the bulls may launch another advance after liquidity is swept below the key lows. However, opening long positions at this stage is not advisable. Traders should first wait for bullish chart patterns to emerge.

At present, traders are monitoring two bearish imbalances, one of which has already been invalidated. At the same time, I would draw attention to the proximity of four significant swing lows that could serve as liquidity targets, as well as the increasingly questionable fundamentals supporting the US dollar's strength. Therefore, I continue to expect a bullish move, but I would first like to see at least some technical confirmation of that scenario. Otherwise, traders should wait for a sell signal to develop within imbalance 17.