English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

You reap what you sow. America has intensified its strikes against Iran, hitting a tanker near the country's main export terminal for the first time since the resumption of the blockade of ports. The target in the depths of the Persian Gulf indicates an expansion of the naval operation. Tehran has fired at American bases in Kuwait and Jordan. Oman reported intercepting eight rockets. Logic suggests that EUR/USD should have plummeted due to such escalation. However, it is rising, surprising both bulls and bears.

Donald Trump threatens Iran with power plants and bridges until it opens the Strait of Hormuz, which has become the center of the war. However, the Islamic Republic is not inclined to back down in the face of the White House's threats. It would seem that the U.S. dollar, as a safe-haven asset, should be celebrating its victory. In fact, the market thinks otherwise, and the culprit is not geopolitics, but the Federal Reserve.

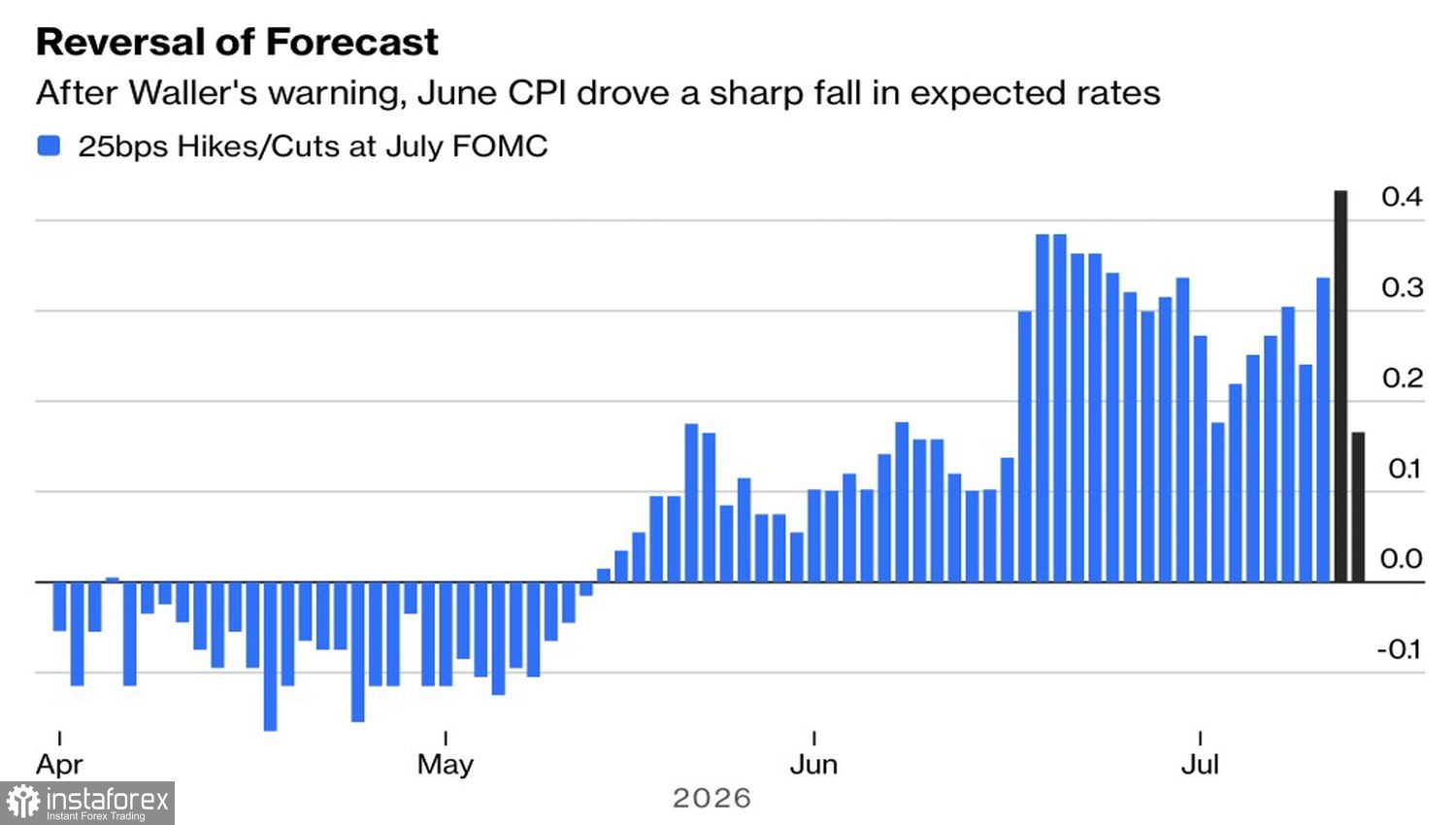

Dynamics of Inflation Expectations in the U.S.

Oxford Economics has summarized the inflationary pressures that never manifested: tariffs, artificial intelligence effects, and the pass-through of oil prices into consumer goods. None of these factors has accelerated inflation as feared by the Federal Reserve. In fact, the effects of an oil shock on prices may take longer to materialize than previously thought.

Annual inflation expectations have fallen below the Fed's 2% target for the first time since the 2024 elections. Investors are betting that Kevin Warsh will quickly overcome price pressures. At the same time, derivatives have dramatically shifted opinions on a rate hike at the end of the month, despite warnings from FOMC Governor Christopher Waller that such a scenario is possible. According to Deutsche Bank, the collapse in expectations following the CPI data was the second largest since the 2008 inflation report. Since Warsh refuses to provide advance signals, such swings risk becoming the norm.

Dynamics of Market Expectations for the Fed Rate

Meanwhile, Goldman Sachs no longer believes in a weakening dollar. The bank has long stated that rates should support the U.S. dollar against low-yielding currencies and has revised its forecasts accordingly since March. Now it has gone further and updated its EUR/USD estimates to 1.14, 1.12, and 1.12 over the 3-, 6-, and 12-month horizons — down from previous estimates of 1.14, 1.18, and 1.20. In its view, the strength of the dollar will persist for a long time. It is too early to talk about a massive collapse.

This creates an interesting paradox. Geopolitics suggests selling the U.S. dollar as a currency losing its status as a safe haven amid a prolonged conflict. Monetary uncertainty, on the other hand, urges buying it in the face of hawkish surprises from the new Fed chair. Which of the two markets will be correct when Warsh decides to surprise investors again?

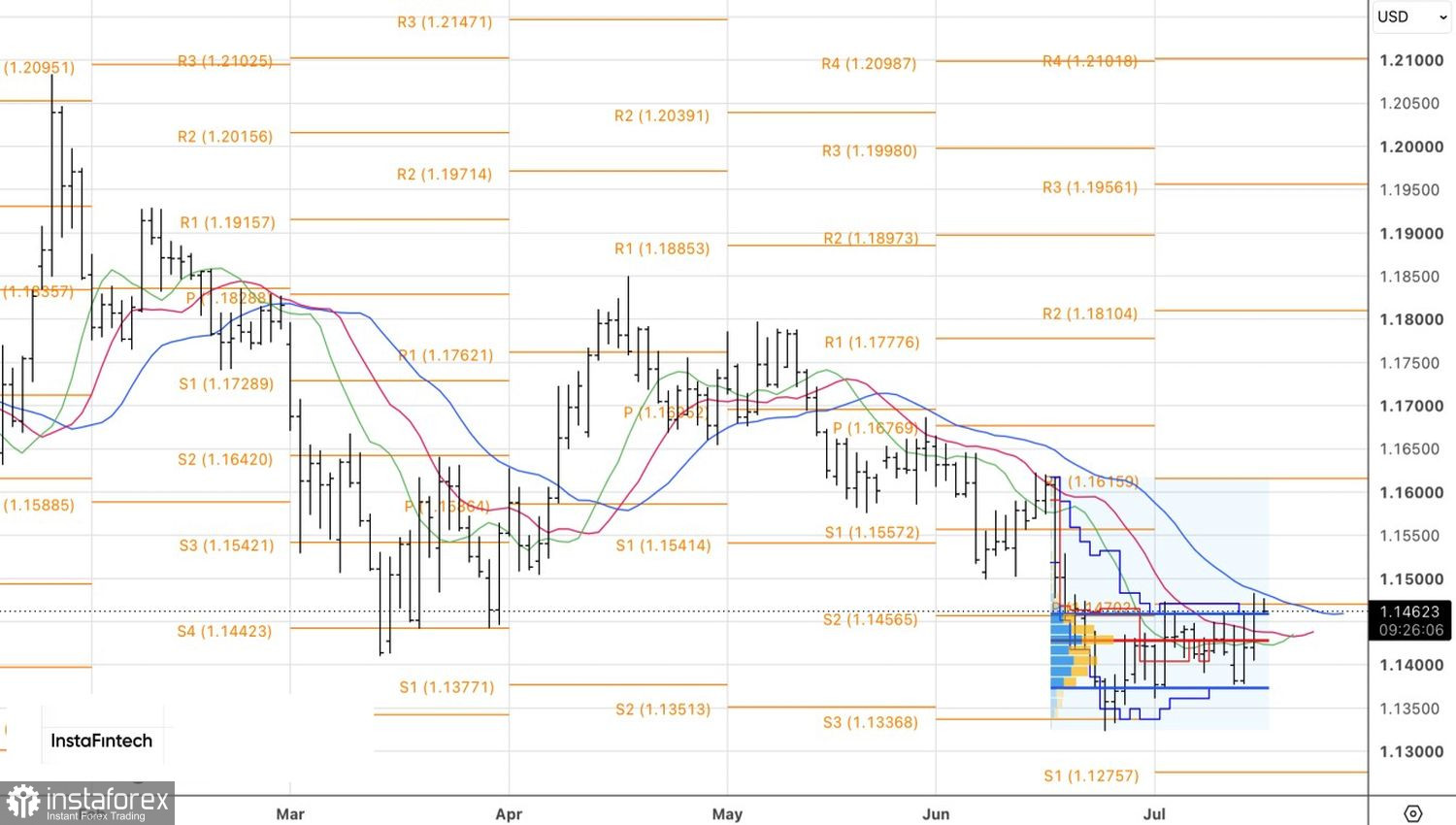

Technically, on the daily chart, EUR/USD tested the upper boundary of the fair value range at 1.137-1.146. If the bulls manage to hold 1.146, the risk of a continued rally will increase. This will allow the long positions formed from the lower boundary area to be amplified.