Tiếng Việt

Tiếng Việt  Русский

Русский English

English Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

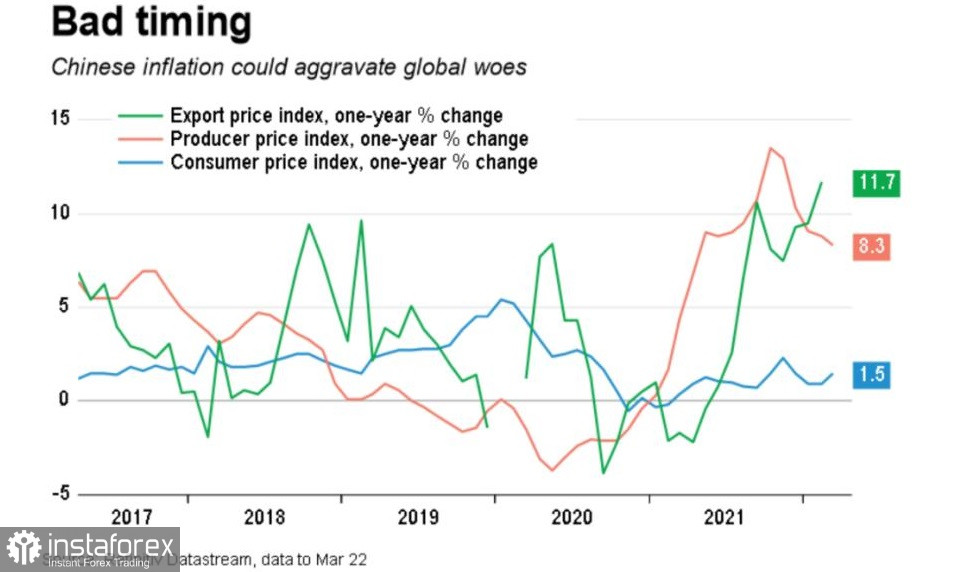

Chỉ số giá sản xuất của Trung Quốc đã tăng 8,3% trong tháng 3 so với một năm trước đó, đánh bại mức dự báo là 7,9%. Các nhà phân tích dự đoán rằng tăng trưởng kinh tế Trung Quốc sẽ chậm lại còn 5,0% vào năm 2022 trong bối cảnh bùng phát COVID-19 mới và thị trường toàn cầu suy yếu, đây là một lập luận bổ sung ủng hộ chính sách ôn hòa.

Châu Á hãy sẵn sàng: Trung Quốc tăng trưởng chậm lại

Tăng trưởng ở nền kinh tế lớn thứ hai thế giới đã chậm lại kể từ đầu năm 2021 do các động cơ truyền thống của nền kinh tế, như bất động sản và tiêu dùng, đã ngừng hoạt động. Xuất khẩu, động lực tăng trưởng chính cuối cùng, cũng đang có dấu hiệu mệt mỏi.

Một số nhà kinh tế cho rằng sự gián đoạn hoạt động trên diện rộng gần đây do đợt bùng phát COVID-19 lớn nhất của Trung Quốc kể từ năm 2020 và việc thắt chặt phong tỏa đã làm tăng khả năng suy thoái.

Văn phòng thống kê của Trung Quốc báo cáo rằng giá tiêu dùng đã tăng 1,5% so với cùng kỳ năm ngoái trong tháng 3 từ 0,9% trong tháng 2. Có vẻ như chính phủ sẽ có một cuộc chiến khó khăn để đạt được mục tiêu 5,5%.

Các nhà phân tích hiện đã điều chỉnh tăng trưởng dự báo cho năm 2022 xuống dưới mức 5,2% dự báo cho tháng Giêng. Dự đoán sẽ còn tăng trưởng lên 5,2% vào năm 23.

Dữ liệu cho thấy tổng sản phẩm quốc nội (GDP) có thể tăng 4,4% trong quý đầu tiên so với cùng kỳ năm trước, cao hơn 4,0% trong quý thứ tư do khởi đầu mạnh mẽ trong hai tháng đầu năm.

Các nhà phân tích tin rằng hoạt động trong tháng 3 có thể bị ảnh hưởng bởi nỗ lực của Trung Quốc nhằm ngăn chặn đợt bùng phát COVID lớn nhất kể từ khi virus Corona lần đầu tiên được phát hiện ở nước này vào cuối năm 2019.

Các nhà phân tích của Societe Generale cho biết: 'Dữ liệu hoạt động trong tháng 3 có thể đã xấu đi đáng kể, nhưng đây sẽ chỉ là phần nổi của tảng băng chìm, vì các hạn chế kinh tế chỉ bắt đầu vào giữa tháng 3', các nhà phân tích của Societe Generale cho biết. 'Tuy nhiên, tăng trưởng GDP thực tế có thể không giảm xuống dưới 4% nhờ sự phát triển cơ sở hạ tầng, phương pháp báo cáo và dữ liệu mạnh mẽ đáng ngạc nhiên trong tháng Giêng và tháng Hai.'

Theo khảo sát, trên cơ sở hàng quý, tăng trưởng được dự báo sẽ chậm lại xuống 0,6% trong quý đầu tiên từ mức 1,6% trong tháng 10-12.

Chính phủ sẽ công bố dữ liệu GDP quý đầu tiên cùng với dữ liệu hoạt động của tháng 3 vào ngày 18 tháng 4.

Xin nhắc lại, GDP của Trung Quốc đã tăng 8,1% vào năm 2021, mức tăng trưởng tốt nhất trong một thập kỷ, nhưng trong năm qua, động lực đã giảm đáng kể do các vấn đề nợ trên thị trường bất động sản và các biện pháp chống vi-rút đã làm suy giảm niềm tin và chi tiêu của người tiêu dùng.

Năm ngoái, các nhà hoạch định chính sách cũng tập trung vào việc kiềm chế rủi ro tài sản và nợ trong nhiều ngành công nghệ cao, làm trầm trọng thêm suy thoái kinh tế.

Lạm phát tiêu dùng cũng dự kiến sẽ tăng lên 2,2% vào năm 2022 từ 0,9% vào năm 2021 và sau đó tăng lên 2,3% vào năm 2023.

Chính sách ưu đãi tiền tệ

Các biện pháp chưa từng có để hạn chế sự lây lan của virus Corona làm suy yếu không chỉ ngành bán lẻ mà còn cả lĩnh vực sản xuất.

Năm nay, chính phủ đã công bố nhiều biện pháp kích thích tài khóa hơn, bao gồm phát hành trái phiếu địa phương nhiều hơn để tài trợ cho các dự án cơ sở hạ tầng và cắt giảm thuế cho các doanh nghiệp.

Chính phủ cũng cho biết hôm thứ Tư rằng Trung Quốc sẽ sử dụng việc cắt giảm kịp thời các yêu cầu dự trữ ngân hàng (RRR) và các công cụ chính sách khác để hỗ trợ nền kinh tế vì COVID-19 có nguy cơ làm suy giảm thêm động lực sản xuất.

Theo khảo sát của các nhà kinh tế, Ngân hàng Nhân dân Trung Quốc (PBOC) có khả năng cắt giảm RRR - lượng tiền mặt mà các ngân hàng phải dự trữ - xuống 50 điểm cơ bản (bps) trong quý 2 năm 2022. Điều này sẽ giúp các ngân hàng tồn tại trong một giai đoạn khó khăn, nhưng cũng sẽ đặt ra một số câu hỏi về khả năng thanh toán của họ đối với các đối tác phương Tây. Có thể một số tổ chức tài chính sẽ nhận được xếp hạng thấp hơn.

Nhưng động thái này cũng có thể làm giảm khả năng cho vay trung hạn sớm, mặc dù lãi suất cho vay cơ bản (LPR) vẫn có thể được cắt giảm vào ngày 20/4.

Các nhà kinh tế tại Citibank kỳ vọng việc cắt giảm 50 điểm cơ bản sẽ được công bố sớm nhất là vào thứ Sáu, giải phóng hơn 1,2 nghìn tỷ nhân dân tệ (188,52 tỷ USD) thanh khoản có khả năng sẽ thúc đẩy nhập khẩu.

Các nhà phân tích kỳ vọng PBC sẽ cắt giảm LPR hàng năm, lãi suất cho vay chuẩn, xuống 10 điểm cơ bản trong quý II, cuộc thăm dò cho thấy.

Lần cuối cùng họ cắt giảm LPR hàng năm 10 điểm cơ bản là vào tháng Giêng và lần cuối cùng họ cắt giảm RRR xuống 50 điểm cơ bản là vào tháng Mười Hai.

Trong hai đợt cắt giảm RRR cuối cùng vào năm 2021, các thông báo nới lỏng tương ứng được đưa ra từ hai đến ba ngày sau khi được Hội đồng Nhà nước ghi nhận.

'Chúng tôi kỳ vọng PBC sẽ cắt giảm RRR 50 điểm cơ bản và có thể cắt giảm lãi suất trong vài ngày tới', Goldman Sachs viết trong một lưu ý hôm thứ Năm.

Hầu hết các nhà dự báo tư nhân hiện dự đoán RRR sẽ giảm 50 điểm cơ bản (bp), giải phóng hơn 1 nghìn tỷ nhân dân tệ (157 tỷ USD) trong nguồn vốn dài hạn mà các ngân hàng có thể sử dụng để thúc đẩy cho vay.

Một bài bình luận từ Thời báo Chứng khoán do nhà nước điều hành cho biết ngày 15 tháng 4 sẽ là một thời điểm đáng chú ý.

Nhìn chung, các biện pháp của Trung Quốc nhằm giảm lượng tiền mặt trong ngân hàng để dự trữ và tăng cho vay làm tăng kỳ vọng của các nhà giao dịch về việc sớm nới lỏng chính sách. Nhưng các nhà kinh tế nói rằng bất kỳ sự nới lỏng tín dụng nào có thể không đủ để chống lại một cuộc suy thoái kinh tế sâu sắc đang rình rập.

Liệu chính sách này có đủ mềm không?

Bất chấp các bước cụ thể nhằm giảm bớt kích thích tài khóa, một số nhà phân tích vẫn đặt câu hỏi về hiệu quả của việc giảm RRR hiện nay. Nguyên nhân là do thiếu nhu cầu tín dụng khi các nhà máy và doanh nghiệp gặp khó khăn và người tiêu dùng vẫn thận trọng trong một nền kinh tế rất bất ổn.

Các kênh truyền dẫn cho RRR thường xuyên và cắt giảm lãi suất đang bị tắc nghẽn nghiêm trọng do đợt phong tỏa liên quan đến COVID và gián đoạn hậu cần, theo Nomura Foundation.

Các nhà phân tích của Nomura cho biết: 'Khi các hộ gia đình đổ xô tích trữ lương thực và các tập đoàn tư nhân ưu tiên sự tồn tại hơn là mở rộng, thì nhu cầu tín dụng sẽ yếu đi."

'Với rất nhiều đợt phong tỏa, rào cản và hạn chế, các vấn đề đáng lo ngại nhất chủ yếu nằm ở phía cung, và việc chỉ cần thêm đòn bẩy và giảm nhẹ lãi suất cho vay là không có khả năng thúc đẩy nhu cầu cuối cùng một cách hiệu quả. '

Các quan chức quỹ cũng cho biết Trung Quốc đang đối mặt với 'nguy cơ suy thoái ngày càng tăng' khi 45 thành phố hiện đã đóng cửa hoàn toàn hoặc một phần, chiếm 26,4% dân số và 40,3% GDP của cả nước.

Lãi suất dự kiến sẽ sớm được cắt giảm 10 điểm cơ bản đối với hạn mức tín dụng trung hạn 1 năm (MLF), lãi suất cho vay cơ bản 1 năm và 5 năm (LPR) và lãi suất repo đảo ngược 7 ngày.

Nhưng đồng thời, lãi suất MLF hàng năm dự kiến sẽ không có thay đổi nào vào thứ Sáu (ngày ngân hàng trung ương gia hạn cho vay trung hạn 150 tỷ nhân dân tệ).

Sau khi cắt giảm mạnh lãi suất chính vào tháng 1, Trung Quốc đã giữ nguyên lãi suất LPR cơ bản hàng năm ở mức 3,70% và lãi suất LPR 5 năm ở mức 4,60%.

Tờ Securities Times bình luận: "Chính sách tiền tệ không phải là thuốc chữa bách bệnh cho mọi vấn đề."

'Mở khóa chuỗi cung ứng và chuỗi sản xuất, cho phép các doanh nghiệp nhận đơn đặt hàng và cho phép mọi người tạo ra thu nhập, sẽ là cách duy nhất để cải thiện dòng tiền của nền kinh tế thực và đạt được sự phục hồi tự nhiên.'

Thị trường toàn cầu có nguy cơ xuất hiện nhiều lỗ hổng mới

Cuộc chiến không mệt mỏi của Trung Quốc chống lại Covid-19 không chỉ thể hiện ở thị trường tiêu thụ và sản xuất trong nước. Nó cũng đang ảnh hưởng đến nền kinh tế toàn cầu, bên cạnh cuộc xung đột ở Ukraine.

Các trung tâm sản xuất và hậu cần của Trung Quốc đang đóng cửa khi các nhà chức trách ngăn chặn những đợt bùng phát mới.

Bất chấp việc đa dạng hóa chuỗi cung ứng, sự phụ thuộc của toàn cầu vào các nhà máy Trung Quốc chỉ ngày càng gia tăng, bằng chứng là số liệu xuất khẩu năm 2021. Tỷ trọng xuất khẩu toàn cầu của Trung Quốc đã tăng lên 15,4% vào năm ngoái, vượt qua mức trước đại dịch là 13,1% vào năm 2019, các nhà phân tích của Bernstein ước tính.

Theo công ty nghiên cứu Gavekal, gần 3/4 trong số 100 thành phố lớn nhất của Trung Quốc, chiếm hơn một nửa GDP của cả nước, đã thực hiện các mức độ hạn chế đại dịch khác nhau kể từ ngày 6/4.

Hầu hết 26 triệu cư dân của Thượng Hải đã bị chặn ở trong nhà của họ trong hơn hai tuần (ban đầu bị cách ly trong 5 ngày), điều này dẫn đến việc đóng cửa các nhà kho và hạn chế tiếp cận cảng container đông đúc nhất thế giới.

Nhà cung cấp iPhone Pegatron đã tạm dừng sản xuất tại hai nhà máy gần đó.

Các biện pháp cực đoan cũng đã được thực hiện vào tháng 3 ở tỉnh Cát Lâm, một nơi sản xuất bắp ngô quan trọng. Các nhà máy của Toyota và Volkswagen cũng được đặt tại đây.

Đổi lại, trung tâm xuất khẩu Quảng Đông đang chuẩn bị cho một đòn đánh khác bằng cách hạn chế đi lại, đóng cửa trường học và triển khai thử nghiệm hàng loạt.

Mặt khác, tập đoàn vận tải biển khổng lồ Maersk đang cảnh báo về tình trạng quá tải các bến container, thiếu xe tải và giảm di chuyển bằng đường hàng không.

Kế hoạch của chính phủ cho đến nay luôn là ngăn chặn hoàn toàn sự lây nhiễm bằng mọi giá. Các biện pháp đóng cửa hà khắc đã cho phép Trung Quốc nhanh chóng khởi động lại các nhà máy sau khi bùng phát sớm vào năm 2020, nhưng biến thể Omicron dễ lây lan hơn.

Than ôi, thiệt hại kinh tế sẽ ngày càng được cảm nhận bên ngoài Trung Quốc.

Những gián đoạn gây ra bởi cuộc chiến thương mại với Hoa Kỳ và sau đó là đại dịch đã khiến nhiều chính phủ và các nhà lãnh đạo phải thảo luận về kế hoạch bảo vệ sự phụ thuộc của họ vào các nhà cung cấp Trung Quốc.

Ví dụ, Giám đốc Ngân hàng Thế giới David Malpass gần đây đã nói rằng đa dạng hóa 'có khả năng mang lại lợi ích cho tất cả mọi người.'

Nhưng cho đến nay nó vẫn chưa thực sự thay đổi nhiều.

Việc ngừng hoạt động kéo dài đối với các nhà máy toàn cầu có khả năng làm giá cả tăng thêm trên toàn thế giới.

Đồng thời, lạm phát ở Hoa Kỳ đã ở mức cao nhất trong 40 năm và giá cả trong khu vực đồng euro đã tăng lên mức kỷ lục 7,5% vào tháng Ba. Giá năng lượng và nguyên liệu thô tăng cũng là nguyên nhân khiến giá bán và giá tiêu dùng của Trung Quốc tăng cao hơn dự kiến trong tháng 3.

Trên thực tế, phong tỏa đã có ảnh hưởng đến thương mại.

Trước đó một tuần, Phòng Thương mại Châu Âu tại Trung Quốc cho biết lượng hàng đến các cảng của Thượng Hải, theo ước tính của họ, đã giảm 40% so với tuần trước.

Nếu các chính sách ngăn chặn virus Corona vẫn chặt chẽ trong năm tới, các thị trường toàn cầu cuối cùng sẽ phải thực sự tìm kiếm các nguồn sản xuất hàng hóa mới, chuyển sản xuất sang các nước đang phát triển khác và nói chung, tìm kiếm sự thay thế cho việc mở rộng thương mại của Trung Quốc.

Trung Quốc sẽ công bố dữ liệu sản xuất công nghiệp và doanh số bán lẻ tháng 3 vào thứ Hai, ngày 18 tháng 4, dự kiến sẽ phản ánh tác động của các hạn chế liên quan đến COVID, cũng như dữ liệu tổng sản phẩm quốc nội quý đầu tiên.